Will Lower Mobile Money Fees in Kenya, Tanzania be Enough to Stimulate Micropayments?

Editor’s note: Jake Kendall, also with the Gates Foundation, contributed to this post.

Many cite the high cost of electronic transfers as a key market barrier to leveraging mobile money platforms and enabling retail payments or other financial services to the poor. (See a previous post on that subject here). But recently, two leading mobile money providers in Kenya and Tanzania lowered their prices for small-value transfers.

Recall that Kenya and Tanzania have the unique distinction of being markets where mobile money has gained the most traction: over 85 percent of adults regularly use M-PESA in Kenya. Tanzania is now home to at least one deployment, Vodacom’s M-PESA, that is successful by global standards, having surpassed 2 million active clients. Nevertheless, uses for mobile money in these markets are still predominantly tied to remote payments (e.g., peer-to-peer transfers and bill payments), where there’s a strong willingness on the part of consumers to pay.

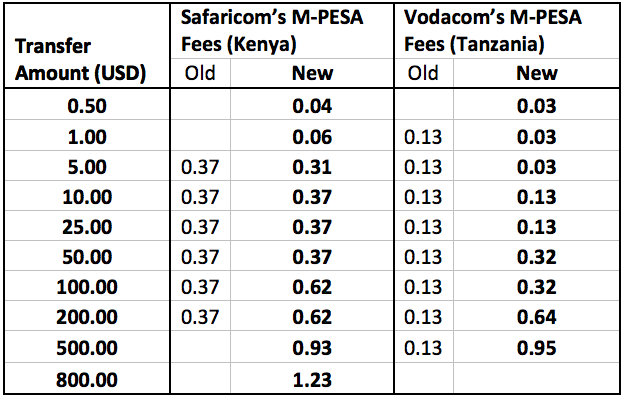

New fee structures for M-PESA in Kenya and Tanzania are tiered to allow for more affordable payments at the low-end, although pricing in Tanzania continues to be more e-money friendly

With this latest move, Safaricom’s M-PESA in Kenya and Vodacom’s M-PESA in Tanzania have enabled smaller transfer sizes than previously allowed (as low as 12 cents in Kenya and 32 cents in Tanzania), reduced transfer fees for micropayments (as low as 4 cents in Kenya and 3 cents in Tanzania), while at the same time increasing fees for higher-value transfers where customers are less price-sensitive.

Indicatively, a 50-cent transfer is priced at 4 cents in Kenya and 3 cents in Tanzania, a $3 transfer is priced at 30 cents in Kenya and 3 cents in Tanzania, and a $10 transfer is priced at 36 and 12 cents, respectively. Note that mobile money transfer fees in Tanzania continue to be significantly less than in Kenya, reflecting the very different competitive environments in which they operate. The table below shows how M-PESA fees have changed in both countries for select transfer values, although other mobile money deployments in those markets have also followed suit.

What do these price revisions mean for financial inclusion?

While much of the media’s attention focused on increased fees at the upper-end, the financial inclusion community welcomes the reduction in fees for micropayments that may enable key use cases relevant to financial inclusion. For example, last September, Jua-Kali, a non-profit pension fund for informal sector workers in Kenya, whose business model relies on “micro-deposits” (daily payments of 25 cents, or weekly payments of no more than a few dollars), was able to negotiate special, lower pricing with Safaricom (ranging from 4 to 19 cents for payments under $12). Such innovative, pro-poor business models would be impossible without affordable and accessible electronic payment mechanisms.

It seems possible that the lower standard prices for all smaller transactions will enable other services like Jua-Kali to leverage M-PESA to serve poor people with their products. However, the prices still go up steeply for larger transfers, which may limit the viability of such services for many wealthier clients, and there are a number of other issues with the M-PESA service in Kenya, including a difficult integration process, which may continue to slow market growth. Thus, we are hopeful but will wait to see uptake before declaring a victory for financial inclusion.

The lower prices in Tanzania seem relatively more likely to engender mobile enabled financial services. However, it is still early days for mobile money in Tanzania and there are few new business models to point to.

Will these price changes enable retail payments?

In neither Kenya nor Tanzania is mobile money being used to digitize retail payments in any significant volume, largely due to the fact that cash is free to use and convenient for in-store payments. Bankable Frontier Associates recently conducted an unpublished study in Kenya to track how people pay for goods and found that 99 percent of transactions are still happening in cash, despite M-PESA’s market penetration. As many as 50 percent of these transactions were under $1-$2 in poor communities. Thus, even with drastically lower prices, cash will be hard to beat.

While the news for financial services is somewhat positive (though, we still have a wait-and-see attitude), it seems unlikely that retail payments will bloom any time soon without even lower prices, and progress on other factors that affect uptake of mobile money for these use cases including user-interfaces, system capacity, and incentives for merchant acceptance. Nevertheless, price may be the “leading indicator” that providers are now more serious about leveraging their platforms for these other payment types going forward.

So we are hopeful to see continued progress on price and other enabling factors in future that can open up the retail payments market. We look forward to seeing how mobile money fee structures will continue to evolve and how such changes will impact usage and functionality, especially amongst the poorest families in East Africa.

- Categories

- Technology, Telecommunications