Caveat Venditor: A New Model for Buyer Selection in Responsible Microfinance Equity Exits

For most, socially responsible investing means just that – investing in a manner that not only generates financial returns but also produces positive social value. But what does it mean for an investor to be “responsible” when selling their holdings? How does one stay responsible at the very moment when one ceases to be an investor?

This is a basic challenge facing investors seeking to “exit,” i.e. sell their equity stakes to a new buyer. The issue isn’t entirely new. It first emerged in the mid-2010s, when several microfinance investment vehicles (MIVs) were starting to reach the end of their 10-year terms and were seeking to divest their assets. This issue was first addressed in the financial inclusion sector by a 2014 paper commissioned by CGAP and CFI, which first defined many of the key questions that socially responsible investors need to address when selling their equity stakes.

With another four years of multiple exits under the sector’s belt, NpM, Netherlands Platform for Inclusive Finance, along with the Financial Inclusion Equity Council (FIEC) and the European Microfinance Platform (e-MFP) asked us to take a closer look at one particularly tricky part of the exit process – selecting a buyer that is suitable for the microfinance institution (MFI), its staff and ultimately its clients. The result is Caveat Venditor: Towards a Conceptual Framework for Buyer Selection in Responsible Microfinance Exits – a new paper that goes beyond raising questions, and seeks to provide a template to help investors navigate the complex terrain of “responsible exits.”

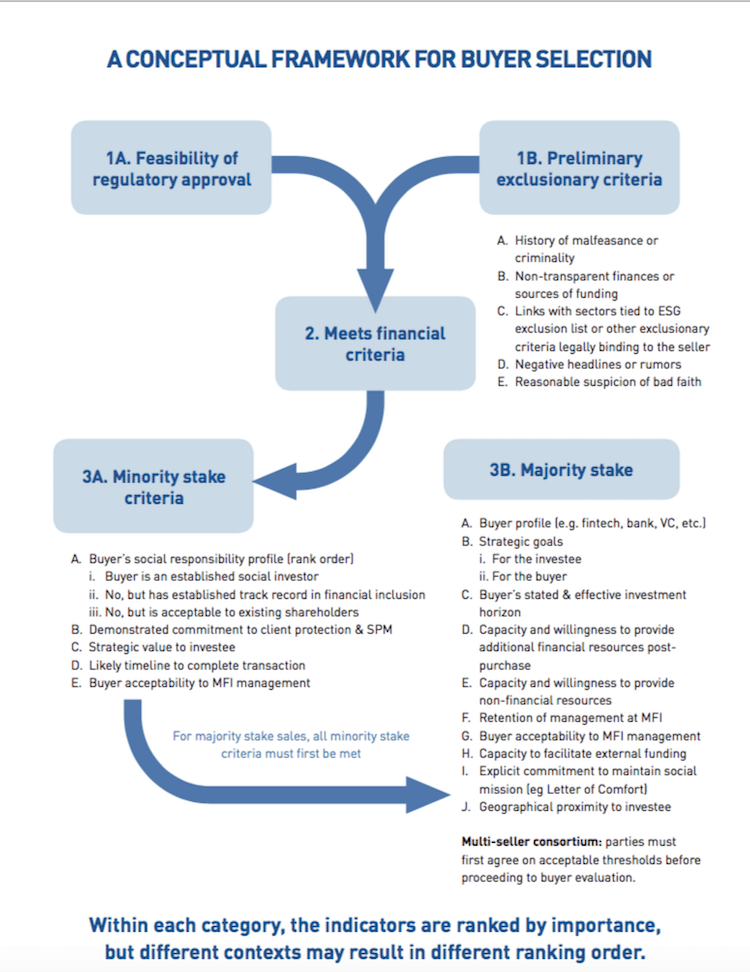

The research – an investor survey, several in-depth interviews and a workshop during European Microfinance Week – found a mix of approaches applied by different investors. But these nevertheless shared many common elements aimed at making sure that the buyer will honor and pursue the social mission of the institution being sold. We consolidated these elements into a “Conceptual Framework for Buyer Selection” – a flowchart representation (plus explanatory notes) of the steps and criteria inherent in responsible buyer selection in microfinance equity exits.

Overall, the consensus among investors was that social responsibility in the context of an exit largely means excluding those potential buyers who are deemed unsuitable and then applying the financial offer (how much a buyer is willing to pay) to select among those remaining. But that exclusionary process is driven by exceptionalism, i.e. buyers have to be obviously unsuitable to be eliminated from consideration, and such exclusions tend to be rare, based on factors like unclear ownership of the buyer, inability to trace the source of the buyer’s funds or suspicion of the buyer’s motives. And because such cases are rare, what this means in practice is that the financial offer is the dominant factor in the decision, much as in the world of purely commercial investors. We refer to this by a term borrowed from medicine, the First, Do No Harm principle.

However, there was an important dissenting view among some investors, which holds that the Do No Harm exclusionary criteria are insufficient for a social investor. After all, a commitment to a social mission is a positive one; it must do good, and not simply avoid doing harm. In effect, this view seeks to invert the process, first deciding whether the financial offer meets the selling investor’s predefined financial objectives, then considering its value to the institution’s social mission. That value need not be strictly mission-driven, nor is there any expectation that the ideal buyers are socially motivated NGOs. Rather, the question is of organizational fit. Extending the medical analogy somewhat, we call this the Best Interests approach. We believe that this model, with its positive obligation on the seller(s), is better aligned with pursuing a social mission while delivering a reasonable financial return – which is at the core of the social investment value proposition.

The framework consolidates the practices of different investors we spoke to but also advocates an evaluation process that moves beyond Do No Harm toward Best Interests while incorporating elements of both. It is structured so that questions are organized based on the type of transaction being contemplated: a minority or majority stake being sold, as part of a consortium of shareholders, or by a single investor.

The framework is not designed to be – nor could it be – one-size-fits-all: Each exit is dependent on the investee’s mission and the context in which it operates, as well as the seller’s own objectives. The framework should be thought of as providing a rubric that each seller can expand upon themselves. It can be thought of as a three-stage process:

- Are there exclusionary factors that mean the potential buyer is manifestly unsuitable; and, if not, is there any reason to believe that regulatory approval for the purchase would be difficult or unlikely?

- If not, is the initial, indicative financial offer within a predefined range that is acceptable to the seller(s) based on the overall double-bottom line objectives of the fund?

- If so, how does the proposed buyer, and its strategic objectives for the MFI, align with the social mission and the other best interests of the MFI?

We believe that the responsibility of finding the right buyer lies very much with those doing the selling. And if the sale means handing over control – a majority stake – this creates an even greater burden. As we argue in the conclusion, “A buyer selection practice which gives primacy to the financial offer and considers social mission and strategic value to the investee – the investee’s best interests – only to reject egregiously unsuitable buyers, fails to keep in mind that the best interests of the MFI and its clients are, for the investors who put funds into the MIV, arguably the primary reason for investing in the financial inclusion sector in the first place.”

We hope this framework will serve as a resource for investors embarking on an equity sale. We hope it could also: help investors to brief external organizations that assist them in exit trajectories (investment banks, advisory firms, etc.); assist new categories of impact investors that have little experience in exits; and serve as a guide to potential buyers to help understand selection criteria and prevent interested (but unsuitable) buyers from wasting time on a futile due diligence process. We hope too that it will inspire further work on an issue which, as equity sales continue to grow, will only increase in importance.

Daniel Rozas and Sam Mendelson are co-authors of the joint NpM/e-MFP/FIEC research project on buyer selection in responsible exits.

Photos courtesy of Pexels and Braden Hopkins via Unsplash

You May Also Be Interested In:

- Categories

- Investing