How Can Fintech Startups Address the Financial Inclusion Gap? Three Insights from the Data Standards for Inclusive Fintech

Significant investment capital is flowing into fintech startups: In 2018, the total amount invested in such startups was estimated to be over US $110 billion, up 120% from 2017. Yet an important question remains: Will this capital help deliver affordable, appropriate and accessible solutions to low-income customers at scale?

Data can help us begin to answer this question – if it is standardized, comparable and gathered at scale. This requires, at minimum, for the industry to collect similar data points and define these data points in the same way. Standardized data is the starting point for creating the data infrastructure necessary to enable investors, fintechs and development organizations to create benchmarks that highlight gaps in current investment flows, surface promising companies, and more effectively define and measure inclusion.

To move closer to this reality, MIX undertook extensive market research in 2019 to develop and iterate upon an initial set of Data Standards for Inclusive Fintech. This market research included over 40 interviews with fintechs, investors and other ecosystem actors, two in-person focus groups, and discussions with our 14-member working group and three-member advisory group. Through the process we surfaced several insights into how to best design and collect information on these data standards, which we compiled in an article published on NextBillion last year. After significant iteration and feedback, we decided late last year to put the data standards to the test: Could we use these data points to create relevant benchmarks for fintechs and investors alike? How might these benchmarks best help both groups understand industry trends – and create the basis for analyzing how fintechs are performing relative to their peers, based on factors such as geography, product and funding stage?

We tested this hypothesis – that data standards can be used to create relevant benchmarks – by collecting data from 45 fintechs via an online survey. The survey form for the data collection was informed by both the data standards and our experience as the implementing partner of the Inclusive Fintech 50 competition. With over 400 eligible early-stage fintech applicants, this competition provided invaluable insight into which sort of data points fintechs were willing and able to share.

Our new report, “Results of the Fintech Benchmarks Proof-of-Concept,” outlines 11 insights, which together illustrate the power of collecting standardized qualitative and quantitative data across a range of fintechs. Below we’ve highlighted three of these insights to demonstrate how this data can help to undercover commercial opportunities for fintechs and investors looking to address the inclusion gap.

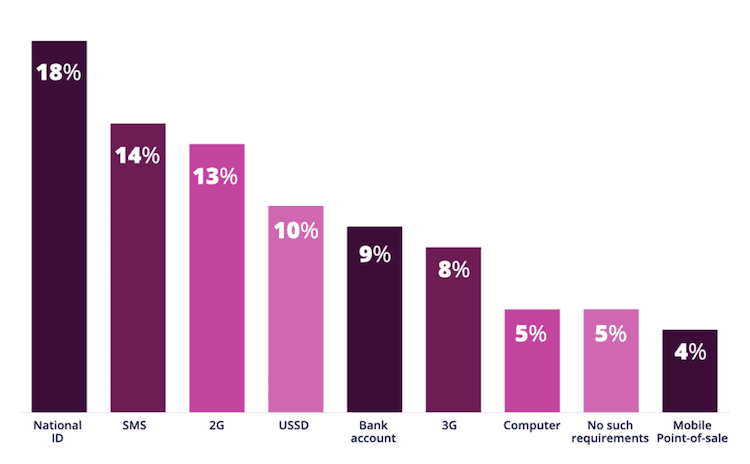

National ID is the main barrier to the underserved

End-User requirements as reported by fintechs

National ID is required at the time of initial registration for 18% of reporting fintechs. This presents a particularly challenging barrier to inclusion, since an estimated 1.1 billion people worldwide do not have access to ID. Since many of those without ID are likely also underserved by current financial services, this suggests untapped growth potential, in that those without national ID could be a potential source of new customers not yet reached by traditional financial institutions or fintech startups. It may also raise questions for investors about how these user requirements could impact a company’s potential to scale. Fintechs might consider how they can innovate to reach new and underserved customer segments despite this barrier. Finally, both fintechs and investors may consider working with key stakeholders, including financial regulators, in specific operating countries to support national-level efforts to address the ID gap.

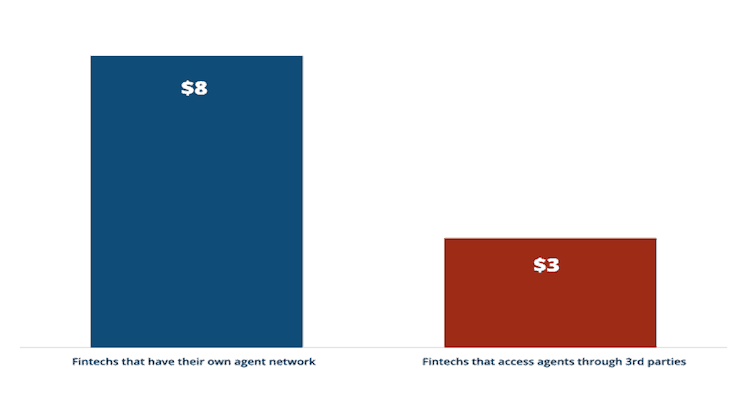

Third-party managers can lower the cost of using agents

Median cost per customer acquisition: staff agents compared to use of agents through third parties

Agents are critically important to expanding financial inclusion: Often, customers who want to use digital financial services – particularly in emerging markets – can do so only if they are able to convert cash into e-money and vice versa. Our analysis found that fintechs in this sample with their own agent network reported having higher costs than those who access agents through a third-party manager. At the same time, fintechs that use any agent network report higher growth rates than those who do not. This signals a strong role for third-party agent managers in emerging markets – and a potential opportunity for investors, as well as fintechs looking to complement their digital services with more face-to-face interaction with customers.

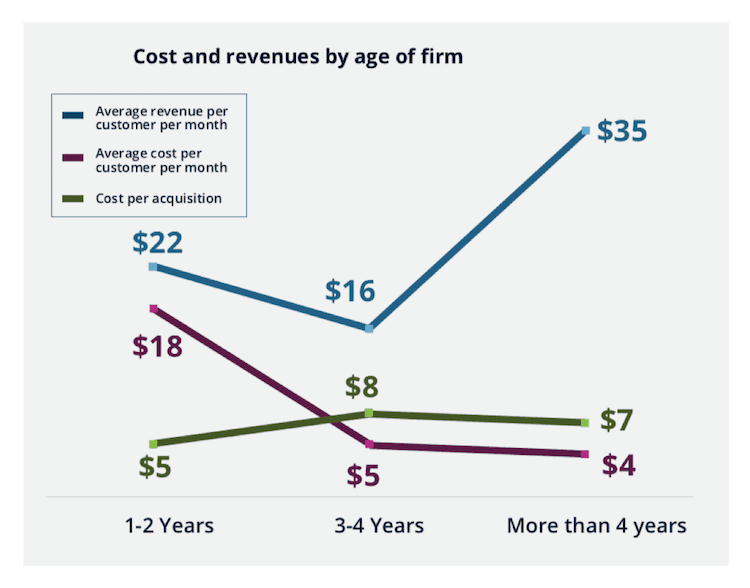

It remains expensive to acquire new customers

Timing is important for any startup – especially when raising funds. Rapid scale happens when a firm achieves product/market fit — signaled by fast growth, high referral rates and low marketing costs. In the data, we can see indications of fintech firms hitting this point after four or more years: But while cost per customer drops by year three or four — suggesting lower operational costs — cost per customer acquisition does not, suggesting that firms are still spending money to get new customers. It also takes longer for referral rates to increase (defined as the volume of referred customer acquisitions as a percentage of total customer acquisitions.) This is an exciting area of future analysis for investors and fintechs alike, as they each try to match investment size and type to the appropriate stage in a fintech’s growth.

What comes next?

We are currently prototyping an online version of RELAY, our overall effort to create the data infrastructure necessary to bridge the information gap between fintech startups and potential investors. Adding to the work we’ve already done on the Data Standards and the Benchmarks Proof-of-Concept report, the RELAY prototype will test how these inputs can be accessed and used within an interactive online platform. The prototype, which will be designed and tested between May and September with support from Catalyst Fund, will provide targeted data and insights to an initial group of pilot users (including fintechs, investors and donors). This will help us better understand the needs and behaviors of both fintech startups and investors as they relate to data.

If you’d like to stay updated on our progress, sign up to receive emails from MIX.

Chrissy Martin Meier is the fintech lead and product manager at MIX.

Photo credit: Sammie Vasquez

You May Also Be Interested In:

- Categories

- Finance