Open the Spigot: The Way We Think About Impact Investing is Too Narrow

A resounding cry heard across many impact investing reports, articles and blogs is that one of the biggest challenges facing the impact investing community is deal flow. The Global Impact Investing Network’s (GIIN) annual report for 2018 noted a key barrier facing the impact investing community is the “limited number of investment ready businesses.” A recent article in Entrepreneur magazine noted “since impact investing, as an industry, is relatively ‘new’, the supply of investment opportunities offering impact, scale, and financial return often falls short of demand.” And the list goes on.

While now a commonly accepted diagnosis, this perceived lack of deal flow is actually the result of a very narrow definition of impact. The issue is not that there is a lack of investible companies, but rather the industry’s detrimentally narrow definition blinds investors to companies that are creating impact in other industries and geographies. We need to broaden this definition by closely analyzing the effects that companies’ products and services have in relation to the eradication of a given social/environmental problem.

Though faulty, this perception is a natural byproduct of the history and rise of impact investment.

History of impact investment

Impact investing was born from the world of philanthropy, which has undergone a steady intellectual shift with regard to international economic development models. What used to be an “aid”-based approach is now an “empowerment”-based approach that focuses on investing in local entrepreneurs that can create local solutions to local problems. (Seminal books such as “Dead Aid” by Dambisia Moyo or “The White Man’s Burden” by William Easterly make this argument).

As a result of these origins, the philanthropy world has largely focused on “wicked social and environmental problems” that plague the bottom of the pyramid (BoP) and, as such, has focused the majority of its efforts within emerging markets.

Traces of impact investing’s philanthropic origins can be seen in some of the leading impact funds: Omidyar Network was founded by billionaire and philanthropist Pierre Omidyar; Acumen Fund is a non-profit impact fund that got its start with seed funding from the Rockefeller Foundation, Cisco Systems Foundation and a handful of philanthropists; Unitus Labs a non- profit microcredit organization which has spun out a number of leading impact funds such as Unitus Seed Fund and Patamar Capital.

With this history in mind, it is no surprise that the trending sectors within impact investing are affordable housing, food and agriculture, health care, education, renewable energy, inclusive finance and women’s empowerment – the same sectors that have long been the focus of international philanthropic efforts.

Further, given the philanthropy sector’s focus on social/environmental issues and emerging markets, it is understandable that the impact investment industry has concentrated on finding companies that create for-profit solutions to these looming issues in emerging economies. And it is these origins that have informed the definition of impact – or at least the perception that ‘impact’ is somehow relegated only to the BoP or to select sectors around the world – and searching for companies in these narrowly defined parameters will result in difficulty finding deal flow.

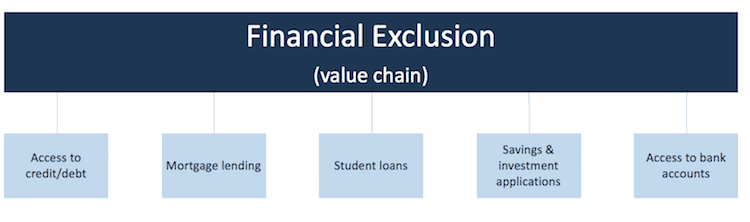

However, this article argues that by assessing, analyzing and understanding how products and services solve the issues that comprise a social/environmental problem’s value chain (see the non-exhaustive diagram below), the definition of impact will expand, resulting in more investment-ready deal flow – as every social/environmental problem is the sum total of contributing sub-issues that sit along its value chain.

Financial exclusion, for example, is not simply a problem that is limited to the BoP in emerging markets. It could theoretically be broken down into sub-issues such as access to credit/debt, mortgage lending, student loans, savings and investment applications, access to bank accounts etc. and these sub-issues affect individuals in both emerging and developed regions of the world. To understand each of these and how they affect their respective ecosystems will open up new opportunities for deal flow in both emerging and developed markets.

The new era of impact investment

Impact investing’s birth from the world of philanthropy was necessary for its existence today, but for it to grow, the industry, along with its investors, must broaden its understanding of impact and find companies outside its traditional geographical or sectoral preferences. This is not an ideological shift, on the contrary, it is an enhancement of the existing ideology of impact investing.

For the impact investing industry to enter this new era, we need to think deeper about the complexity of the issues at hand and develop granular understandings of how various models and technologies tackle specific sub-issues within their respective contexts.

To look at how technologies such as smart cities or internet of things can help reduce pollution in both developed and emerging cities, how diagnostic disease treatment apps can identify health problems of people across the socio-economic strata (not just the BoP), how clean technologies can create sustainable energy for major corporations to rural slums, how agriculture technologies can increase crop yields for farmers both commercial and subsistence across the world, how fashion brands can create ethical and sustainable clothing for all market segments; that is what will contribute to the broadening definition of impact, and subsequently the scope for deal flow.

If impact investing’s goal is to create sustainable and impactful change, then it will require a holistic approach, not merely a plug and play approach. In furtherance of this lofty goal of systemic change, companies of all sizes, in all sectors, will need to shift their focus toward the creation of impactful and sustainable products and services. As an investor, widening the definition of impact by understanding how various products and services contribute to this systemic change, and analyzing how these products and services tackle sub-issues of social/environmental problems, will enable more deal flow to appear and greater impact to occur.

Tanner Taddeo is the Vice President of ChangeSquare.

Image courtesy of Pixabay.

You May Also Be Interested In:

- Categories

- Investing