Making it Easier to Go Digital: Lowering barriers to entry for pro-poor financial institutions in Uganda

In December 2014 Airtel Uganda launched a mobile banking service to allow bank customers to access their accounts through mobile money agents. Since then Airtel and MTN, mobile network operators (MNOs) that control nearly 99 percent of the mobile money market in Uganda, have enabled access to mobile banking services for six financial institutions.[1]

These services have opened up a new channel that can allow microfinance and other financial institutions to reach rural Ugandans who live too far from bank branches. In a market like Uganda, where 14 percent of the population has a formal bank account yet 33 percent has a mobile money account, the benefits of this access are clear for customers. They can use their mobile phones to move value between their mobile wallets and bank accounts. And since mobile money agents are located closer to where they live and work, customers save time and transportation fees when conducting financial transactions.

But for financial institutions, forging these connections is more complex. Connecting financial institutions and operators requires merging technical systems that are not always easily compatible. And though some larger institutions have made the investment, many pro-poor institutions have lacked the resources and capabilities to do so.

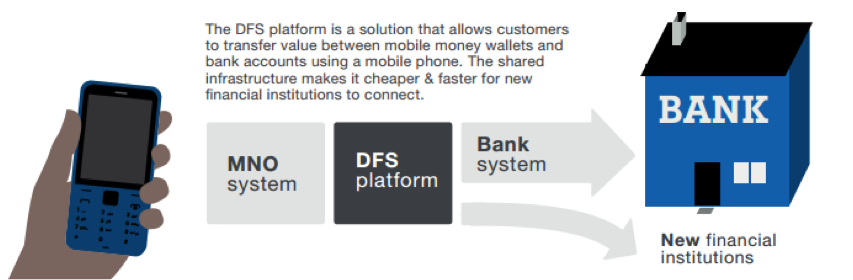

One objective of the Grameen Foundation’s Mobile Financial Services Accelerator program is to provide a platform that addresses this market need by reducing the barriers to entry for pro-poor financial institutions. (Note: Grameen Foundation is a NextBillion content partner). Through an engagement with Cellulant, a mobile payment and digital commerce platform provider, we have designed a Digital Financial Services (DFS) platform that has helped our partners, Centenary Bank and Pride MDI, connect to the ecosystem. The platform comprises three elements:

- Distribution Rails: Instead of a “stovepipe” (one-to-one) technical approach that is often followed by integration software providers and/or service vendors, the DFS platform provides all of the required connections via a shared infrastructure that enables multiple options for getting “on board,” to help new institutions quickly offer services over the mobile money channel;

- Connection Processes: Institutions are provided with step-by-step documentation on processes to simplify the connection process, including both technical and operational considerations (such as funding and monitoring reconciliation accounts);

- Product Design: Not all product business rules are best placed in the core banking system, where changes can be very expensive. The DFS platform is a place where business rules for new products can be built to avoid costly changes to core banking systems, and a “sandbox” testing environment that makes the creation and release of new products easier and faster.

Above: Diagram of DFS solution

Though this platform can facilitate some processes, going digital still requires a re-examination of other long-standing assumptions and processes with financial institutions. Here are some ways pro-poor institutions can manage this:

- Creating a Winning Engagement Model: Project team members are a scarce resource. Digitizing products for the first time can be a time-consuming, potentially all-encompassing endeavor. The exercise is particularly difficult for pro-poor financial institutions that operate using a high-touch, low profit margin model. Organizations should balance who is needed and when. Create a smaller core team; focus not only on activities and milestones, but also on how to engage staff throughout the project.

- Isolating the Technology: The technology work involved in opening digital channels should be separated, and its success can’t be assumed. The best technology applications are developed through specific use cases and strong support for developing requirements and testing solutions. Create a separate work stream for the technology integration that provides connectivity before fully engaging the other business functions within the organization, such as human resources and marketing. Also, invest in integrating the technology infrastructure, both the physical connections (such as required virtual private networks [VPNs] or leased lines) as well as a sufficient level of application-level integration (such as confirming the availability of required data parameters), to prove feasibility and provide demonstration and test platforms.

The development of the DFS platform in Uganda aims to address these internal challenges by creating a simplified process and guides that make it easier for financial organizations to join. Additionally, to ensure that pro-poor institutions of all sizes are able to afford to access the system, Cellulant offers a basic package of services (simple deposits from mobile wallet to bank accounts, and withdrawals from bank accounts to mobile wallet functionality) at a significant reduction in joining costs.

We examine in further detail some high-level learnings in our DFS Lessons Learned document. For more information on the platform, contact Felix Nthigah (felix.nthigah@cellulant.com).

[1] Airtel’s menu includes: Equity, Centenary, Pride, Opportunity, DFCU. MTN’s menu includes: Centenary, Stanbic, DFCU, Pride

Lisa Kienzle manages global operations and strategy for Grameen Foundation’s financial services initiatives. Leo Tobias is the Technical Program Manager for the Grameen Foundation Microsavings project.

- Categories

- Uncategorized