Microfinance for Refugee Populations: What We’ve Learned and Where to Go Next

Refugee populations have been present throughout human history, in countries all around the globe. The long, brutal and ongoing civil war in Syria and resulting migrations of Syrian refugees have, however, increased international focus on the challenges that refugees and their host countries face, as well as on how communities at the local, national and international levels can and should respond.

Currently, 21.3 million people are registered with United Nations agencies as refugees, 75 percent of whom have been displaced from only seven countries: Palestine, Syria, Afghanistan, Somalia, South Sudan, Sudan and the Democratic Republic of Congo. But they have fled to 169 countries. One of the many facets of this complex situation is the financial needs of refugees. Meeting these needs, as we know already from the microfinance sector, is inextricably entwined with addressing many of the other fundamental challenges experienced by vulnerable populations related to self-sufficiency, safety and hope for the future. Financial inclusion of refugees is thus a matter of both importance and urgency.

The Social Performance Task Force (SPTF) began collaborating with the United Nations High Commissioner for Refugees in 2015 to define in detail the financial needs of refugees, identify the reasons why the financial sector thus far has largely failed to meet those needs and propose some possible solutions. As a first step, SPTF hired independent consultant Lene Hansen to review the studies and literature published to date, to conduct a series of interviews with experts – including practitioners working on this topic – and to visit, analyze and write a case study on a financial service provider (FSP) that has been extending its services successfully for years to refugees, and to develop guidelines for FSPs based on all of this collective research. These guidelines, “Serving Refugee Populations: The Next Financial Inclusion Frontier,” are now available from the SPTF website.

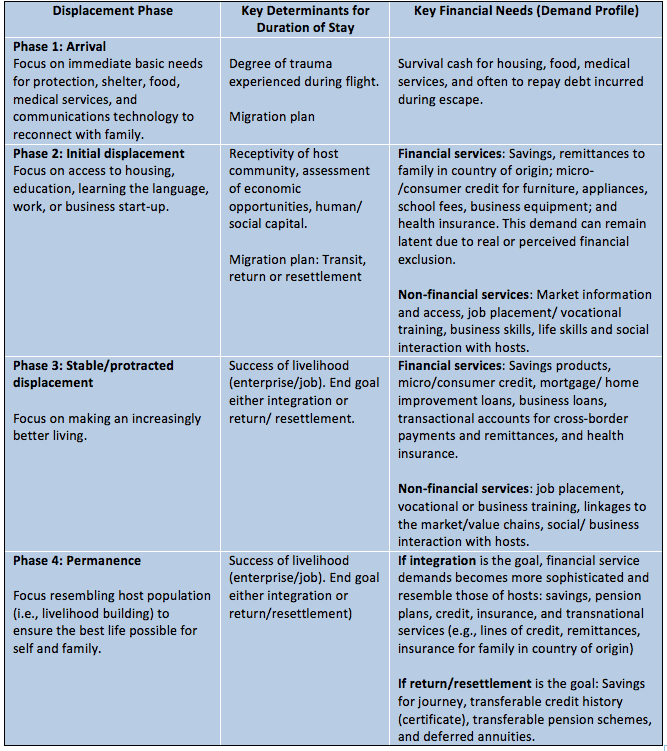

A clear lesson that emerges from SPTF’s work is that refugees do have financial needs, but those needs vary significantly according to their current phase of displacement and migratory plans for the future. For example, refugees who are newly displaced are very likely to demand remittance services and a safe place to save their money, but will likely have minimal demand for loans. However, demand by refugees in stages of protracted displacement or permanent relocation mimics that of national clients; namely, demand for the full range of financial service products including remittance services, savings, insurance and loans. The table below summarizes key financial needs by displacement phase:

It is important to note that, for a refugee in any stage of displacement, there is no refugee-specific financial product that an FSP must develop. In fact, FSPs should be very careful to offer the same terms and products to refugees and to nationals, so as not to breed resentment among the two groups.

On the other hand, much work will likely be required, both within the FSP and by stakeholders external to the FSP, to combat misperceptions and prejudices, and change exclusionary regulations and policies so that financial inclusion of refugees is possible. For example, one of the many misperceptions commonly held by FSPs is an assumption that refugees are highly mobile and therefore pose a flight risk. Other assumptions are that they are too poor, that they do not have the skills to run a successful business, that they are too difficult to reach because they live in camps, and that serving them involves such high costs that it could not be profitable. In fact, the majority of refugees are not mobile (56 percent of refugees have been in displacement at least 10 years), they are already economically active, two-thirds of refugees do not live in camps and the portfolio-at-risk figures that we do have on refugee clients show that they have very low delinquency rates. It must be mentioned, though, that the risk mitigation measures taken on lending to refugees have in some cases been particularly conservative.

Regarding external stakeholders, many obstacles arise from the laws and regulations of the land that prohibit FSPs from extending services to refugees and/or make it very challenging for refugees to engage in income-generating activities. Some examples are legal restrictions on the mobility of refugees, prohibition of access to markets, non-issuance of work permits, and the requirement to have a national ID to open a bank account. Another critical external stakeholder is the body of existing national clients, who may initially be quite hostile to the idea of having their FSP extend its services to refugee populations for fear that any capital loaned to refugees means fewer funds available for national clients, and/or that the loans provided to refugees could enable them to open businesses that would compete with the businesses operated by the nationals.

Additionally, the strategy for outreach and marketing to refugee populations will likely need to be quite different from the one the FSP uses for national populations. First, FSPs will have to learn how to find refugees in their communities. Often, they simply do not know. And once they do become informed, it is still doubtful that direct outreach would be fruitful, due to cultural, language, and trust barriers. Instead, it can be more effective for the FSP to conduct its outreach via an intermediary body that has already been working with refugees, such as a local community center. Non-financial services will also likely be critical, because of their potential to build trust and acceptance among all parties and to enable the refugees to integrate (e.g., language lessons), as well as to build financial skills.

The question of what to do next is under intense discussion by stakeholders around the globe. SPTF has already participated in several meetings of donors, investors, governments, practitioners, and other concerned stakeholders, to make each other aware of our current efforts, discuss ways to coordinate and collaborate, and debate next steps. These discussions are ongoing, but SPTF has already committed forming a working group that will be open to all and hold online webinars every two-three months over the next year. We hope to highlight examples of practice, share findings from new research, and facilitate discussion and collaboration among the various actors in this space. If you would like to participate, please email info@sptf.info.

Amelia Greenberg is the deputy director of the Social Performance Task Force.

Photos of refugee entrepreneurs at a camp in Rwanda, by Amelia Greenberg.

You May Also Be Interested In:

- Categories

- Finance