‘Cross-sell Done Well’: How One Finance App Found a Balance Between Digital and Human Touch

Field officers at Sajida Foundation, an NGO and microfinance provider in Bangladesh, are constantly on the go. They each have over 300 customers to manage: They are responsible for disbursing loan payments, ensuring timely repayment, and in addition, they make up to half a dozen personal visits each afternoon. These officers also act as financial advisors to many of their clients, who they get to know well over time. But the reality of their workload doesn’t allow them to spend more time coaching clients, which is an activity many enjoy and that clients benefit from.

Field officers understand their clients have rich financial lives, with needs, aspirations and goals for the short and long term. Some clients hold sizable savings balances as they seek to save for these goals. Officers know their clients could earn more by converting those savings to a term deposit account. Yet, in many cases, advice-giving is complex: It is difficult for officers to answer questions around tiered interest rates and to identify the right customer profile to offer differentiated products.

An Opportunity for Efficiency: The FAS App

As an OPTIX partner, the SAJIDA Foundation in Bangladesh worked with BFA to find a way for field officers to put their knowledge and intuition about clients to better use and to increase their efficiency. The solution is an Android-based Financial Advisory Services (FAS) app for field officers that identifies “super-savers” and provides officers with useful simulation tools. The FAS app was piloted in two branches and is now being deployed to other branches.

SAJIDA Foundation’s decision to develop the FAS app grew out of two realizations:

- Identifying “super savers”: “Super savers” are individuals who save diligently while servicing a microcredit loan, thereby accumulating a large amount in regular savings without making any withdrawals. Yet information on “super savers” is not readily available to field officers during field visits, which focus on loan servicing and information collection.

- Product simulations: Target-based narratives are a good start to discussing term deposits, but field officers had a difficult time answering questions about expected income based on tiered interest rates, particularly if members were aiming for a specific amount or comparing returns with competing offerings from other institutions.

FAS App in Action: Identifying Super Savers

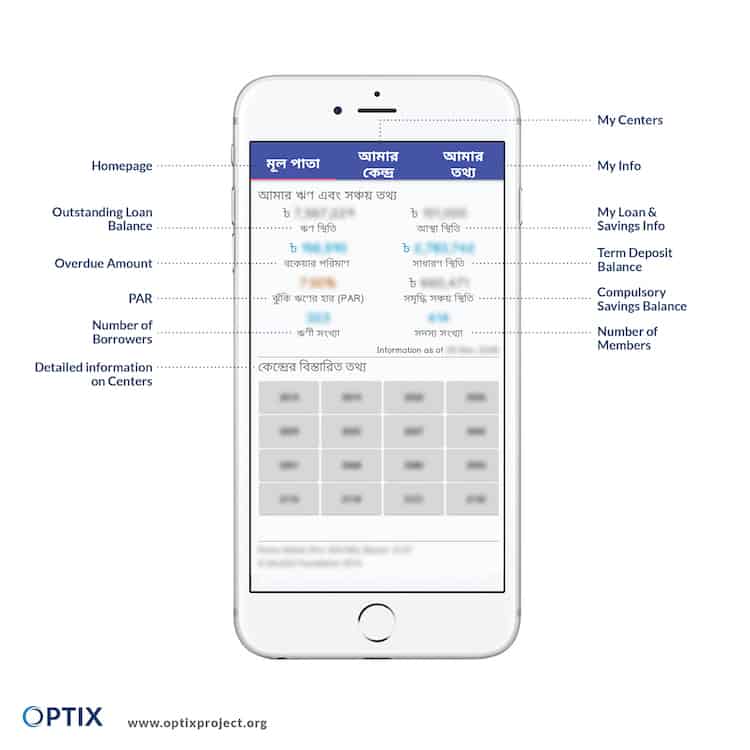

The app’s landing page gives field officers a summary of clients’ loans and savings balances, as well as delinquent loans. Like the SAJIDA Foundation’s collection sheets, data is pulled directly from the SAJIDA databases in English, while the labels are in Bangla, making the interface intuitive for loan officers.

Figure 1. Portfolio Summary (Displays: Outstanding loan balance, balances of three savings accounts, PAR rate, and number of clients).

Figure 2. Center Summary (Displays: Member-wise list with indicators for quality of loan and savings, and length of membership).

The Center Summary, like a dashboard in the app, displays a list of all the members in that Center, along with the status of any current loans and savings. (Fig 2). The app categorizes clients into 1, 2, or 3 stars.

- Three stars: Members who have more than Tk. 10,000 (USD 125) in their voluntary savings account, and have not withdrawn for more than a year. These “super savers” are the primary targets for term accounts.

- Two stars: Those members who have between Tk. 5,000 (USD 62.50) and Tk. 10,000 (USD 125) in voluntary savings, and have held that balance for more than a year. They are secondary targets, who may be engaged in a conversation about long-term goals and term deposit accounts.

- One star: Those members who have between Tk. 4,000 (USD 50) and Tk. 4,999 (USD 62.50), and have not withdrawn in more than a year. These clients are clearly savers, but have not yet achieved the minimum balance for term deposits. Field officers coach them in considering their long-term goals and encourage them to save the minimum level.

Figure 3 Target Savings Page

The Center Summary also notes the status of all outstanding loans in the group. Loans have three states: good, overdue (i.e. somewhat behind on payments), and bad (i.e. recovery efforts have failed, and will be written off soon).

The Summary allows field officers to quickly identify members with three stars and “good” loans, to efficiently zero in on those who may be interested in flipping from savings to term accounts.

From the Summary page, clicking on any member takes the field officer to a page with details on: current and previous loans; balances of compulsory, voluntary, and term deposit savings; and the option to see more details such as choosing a new savings goal to simulate.

These client histories help officers as well as members, who appreciate being able to see their entire portfolio at a glance. In addition, the stars seemed to have a motivating effect for clients, an unexpected but welcome side-effect.

“Wow, Ma, you have three stars!” crowed Nilufer Begum’s daughter, as she and her mother pored over a handheld screen showing her loan and savings records with SAJIDA Foundation. Next to them, the field officer, Arif, explained that three stars were reserved for the best of SAJIDA Foundation’s savers. Using the 3-star system, he advises her on transferring some of her savings to a term deposit account to earn more interest.

Savings Simulations

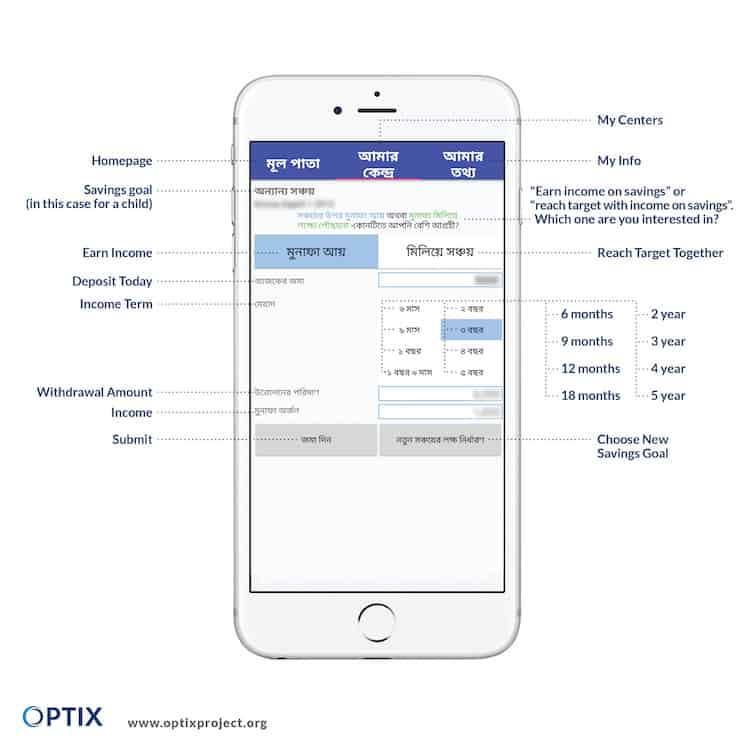

The FAS app offers two simulation tools: (1) one based on more general income generation and (2) a target-based one. These allow officers to work with their clients and show them possible future scenarios, telling them either how much they would save after a certain amount of time, or how long it would take them to save up for something specific.

The Term Deposit Income Calculator:

Figure 4. Simulation: Income Generation (Displays: Maturity amount and income received, given initial deposit and term).

This tool allows field officers to show someone who has a certain amount of idle cash how much they could earn with a term deposit account. Before the app, officers used a grid to show returns based on a few initial deposit amounts and terms, but the app allows them to use a specific amount that is relevant to the client, to produce potential income figures in less than a minute.

The typical term deposit value solution offers a higher rate of interest income than current accounts, with increasingly higher rates for longer committed terms. Thus, someone saving Tk. 10,000 (USD 125) for two years will receive 7 percent per year, resulting in an income of Tk. 1,400 (USD 17.50), and a total withdrawable amount of Tk. 11,400 (USD 142.50).

The Target-Based Savings Calculator:

During discussions with clients, they asked questions like, “If I needed Tk. X in three years, how much do I have to save now?”

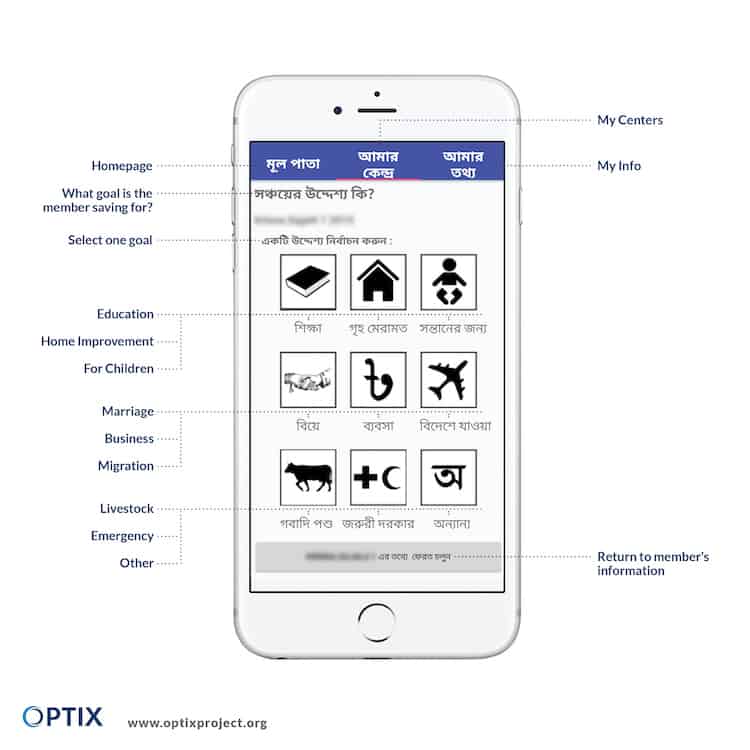

Target-oriented savings pitches are more tangible for users and Sajida used focus groups to develop nine goal categories: education, home improvement, children, marriage, business, migration, livestock, emergencies, and other. When considering target-based savings, the officer inputs how much the client would like to withdraw at the end of the period, and the simulator calculates how much has to be deposited today to generate that amount.

For example, to withdraw TK. 10,000 (USD 125) in two years, one would have to deposit Tk. 8,772 today (USD 109.65), which would earn Tk. 1,228 (USD 15.35) in interest over the two years, allowing the member to meet her target.

Figure 5. Simulation: Target-based Saving (Displays: Initial deposit required and income received, given target maturity amount and term).

Reflections on Cross-Sell and Next Steps

The FAS App was designed to provide field officers with client information in a user-friendly manner to prioritize outreach, and facilitate conversations around various saving and income-generation scenarios. The three-star rating system for savers allows field officers to tailor their advisory sessions, and members seem to appreciate achieving the highest tier with three stars. The eight savings goals represent a simple but powerful distillation of on-the-ground qualitative work, UI (user interface) design and UX (user experience) feedback. The dual simulation modes of Income Generation and Target-based Saving cater to the two predominant lenses through which members view term deposits.

SAJIDA Foundation accomplished what it set out to do: give its staff the right tools to ease their jobs, to have better conversations with clients and a way to more effectively serve the needs of existing clients with tailored term deposits. Field officers are now empowered to have knowledgeable conversations as trusted financial advisors. The FAS app is a great example of cross-sell done well and the right balance between technology and human touch.

Next Steps

The SAJIDA Foundation and BFA will refine the simulation narratives based on the occurrence of target-based term deposits vs. income generation ones. We will also determine the ROI of the FAS app by looking at the number of new term deposit accounts and increased efficiency among field officers. Stay tuned as we keep iterating and give you more updates!

Ashirul Amin is a senior associate at BFA.

BFA and MetLife Foundation created OPTIX to support financial institutions in building better portfolios of products for their low-income customers. Starting in 2016, OPTIX has partnered with four financial institutions in Mexico, Colombia, Vietnam and Bangladesh to understand and advise on the benefits of cross-sell strategies for the businesses and their clients.

Photos courtesy of BFA.

Main/homepage photo credit: Japanexperterna.

You May Also Be Interested In:

- Categories

- Finance, Technology