Not Just Another Startup Accelerator in India: How the Financial Inclusion Lab is Shining a Light on Underserved Customers

This blog talks about the Financial Inclusion Lab accelerator program, which is supported by some of the largest philanthropic organizations across the world – Bill & Melinda Gates Foundation, J.P. Morgan, Michael & Susan Dell Foundation, MetLife Foundation and Omidyar Network.

India today has an accelerator for almost every domain, ranging from fintechs to Internet of Things (IoT), from healthcare to consumer retail. You name it, we have it. It often seems that there is an accelerator in every corner of India’s major cities, with a new one springing up every month.

So why am I writing an article on another incubator/accelerator in India’s fintech domain?

The reason is that many accelerators face a common shortcoming: inclusivity. So when an accelerator comes along that addresses that issue, it’s worth noting.

The Indian fintech ecosystem has still not been able to reach underserved communities, especially the low- to medium-income (LMI) population of the country—households that earn between US $2-10 daily, with volatile and unpredictable incomes. A huge digital divide plagues our society, and few seem to care about it.

We at MSC decided to take it upon ourselves to create an impactful support system to boost the nation’s progress toward financial inclusion, and build a legacy that relevant ecosystems in India and other countries can benefit from. To that end, MSC conducted an intensive landscape study on the startup ecosystem to determine the type of support that could be given to startups to strengthen the financial inclusion movement in India.

As a result of these deliberations, the Indian Institute of Management Ahmedabad’s Centre for Innovation Incubation and Entrepreneurship (CIIE.CO) set up the Financial Inclusion (FI) Lab under the Bharat Inclusion Initiative in 2018, with MSC as a partner.

Lessons Learned from the FI Lab So Far

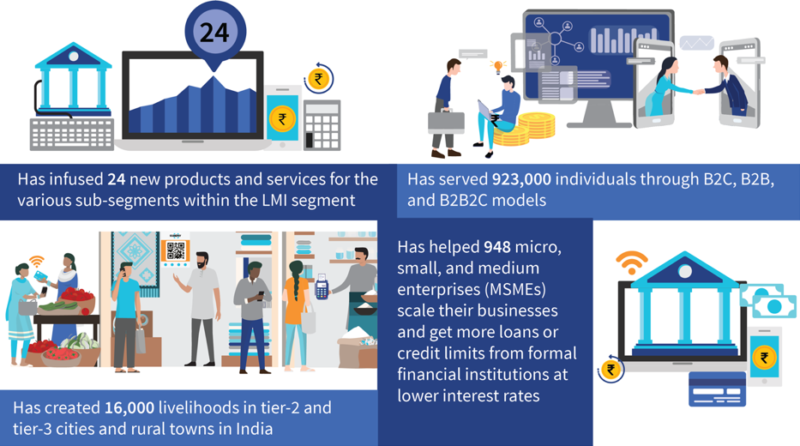

The Lab offers a holistic package of support for each startup, ranging from mentor hours and grant capital to field studies led by financial inclusion experts for consumer and market insights. Since its inception, the Lab has successfully supported 18 startups across two cohorts, and is currently running the third cohort of startups. These startups are from diverse domains of financial services, from savings to insurance to agri-finance. The infographic below depicts the combined impact of our lab.

Source: MSC Analysis (as of December, 2019)

While these numbers appear quite impressive, serving these startups has been challenging. In the process, we have learned six lessons about how best to provide technical assistance to them. We have also learned or reinforced three fundamental lessons for the ecosystem.

No one-size-fits-all solution: One-size-fits-all solutions will not work across the LMI segment. To take just one example, one might expect that women self-help groups (SHGs) would share enough similarities across geographies that a standardized approach could work for them all. But in Pune’s suburbs, these SHGs’ members can pay their households’ dues using smartphones and mobile apps. On the other hand, many SHGs in Rajasthan’s towns include users who only own basic feature phones. This means that an intuitive mobile solution designed for Pune’s SHG customers may be too complex for Rajasthan’s SHGs.

Beware of copy-paste solutions: Most of the startups building solutions for the LMI segment simply extend the solutions they’ve developed for urban, tech-savvy folks—a classic copy-paste approach. For instance, so many Indian mobile apps use a “shopping cart” icon, which blue-collar factory workers or people living in tier–II cities who have never seen a supermarket or a cart cannot relate to or identify.

Founder participation in Lab activities helps them build faster, superior solutions: The Lab was able to give its startups a deeper understanding of the LMI segment, and challenge their solutions and their applicability to LMI customers. This provided new understanding – and prompted new thinking – among many of our enterprises. For instance, the EasyPlan founding team, during its participation in the Lab’s field research activities (such as customer interviews and market surveys), realized that its solution was not a fit for its target customer segment. It quickly adapted to build a new product-market fit for a new LMI customer segment that would buy its products willingly.

How is the Lab Unique?

There are several reasons why the Lab’s approach is uniquely suited to helping startups serve LMI customers.

We start from where others have left off: Many startups and accelerators stop at the point of creating a product or service they think will serve the LMI segment and fulfill the objective of financial inclusion. For us, that’s just the starting point. Once these products and services have been created, we work with startups to help them customize and implement their solutions with their LMI customers. For example, Navana Tech builds a text-free, image-based and voice-enabled software development kit (SDK) for the LMI segment. Navana Tech’s clients build intuitive, user-friendly mobile apps leveraging this SDK to cater to their LMI end customers, such as smallholder farmers, micro-loan borrowers, etc. We helped Navana Tech build image-based mobile applications by validating their mobile user interfaces with actual target end-users.

We support startups to support themselves: While most of today’s accelerators have become intermediaries that merely connect startups to venture capital funds, we believe that startups should first be mentored to build self-sustainable businesses that will become investable.

We understand the LMI segment: period: Many fintech accelerators focus on financial inclusion but have limited knowledge about the nuances of the LMI segment. Since this population comprises the core customer segment for financial inclusion, these accelerators are unable to provide the required support. All the startups from our cohort believe that by working with us, their understanding and sensitivity towards this segment has increased manifold.

Credibility is the name of the game: We have brought together credible partners and CSR grant money. Additionally, a high-level advisory and steering committee has provided further credibility, along with helping startups avoid any regulatory pitfalls. As a result, joining the Lab signals that they are a part of an authentic portfolio of impact investors. This has helped many of them to raise funds more easily.

Gender diversity: We are proud to support startups that are led by women founders. This shows in the rich mix of our selected startups, wherein more than a third of them have women co-founders. The “ladies in the lead” hold the mantle of their respective businesses through their roles as chief executives to chief marketing to chief technology officers.

The Lab actively promotes India’s technology infrastructure: India Stack, the world’s largest application programming interface (API), helps startups reduce the development costs for APIs by 90%, as compared to developing or using other commercial APIs. The Lab also mentors and supports its startups in utilizing this infrastructure, and helps to strengthen it through more avenues of innovation by building a diverse range of solutions on top of the stack.

FI Lab’s Response to the COVID-19 Pandemic

As I write this article, the COVID-19 crisis has started to affect India’s startup community badly. In brief, these are some of the major challenges facing the country’s startups as the pandemic unfolds:

- They have had to completely shut down field operations, including onboarding new customers through physical visits.

- Their revenue streams have shrunk, because customers are delaying or even refusing payments.

- Their suppliers have started asking for pre-payments, and have stopped giving credit.

- There is no government or regulatory support ready yet for fintech startups.

- Startups are looking at cost-cutting measures more actively than ever.

MSC and the Centre for Innovation Incubation and Entrepreneurship have been modifying our approach to offering high-touch support to help the Lab’s startups navigate these troubled times. Some of the measures that we have initiated already include:

- Maintaining the flow of field-based insights to startups by re-working our strategy of conducting research — from on-site field research exercises to telephonic and remote interviews.

- Coaching startups to automate their internal processes and digitize communication channels with end customers.

- Building short-term (1-4 months) and medium-term (4-8 months) contingency plans and strategic roadmaps for startups

The Lab’s Evolving Focus for Fintechs in India

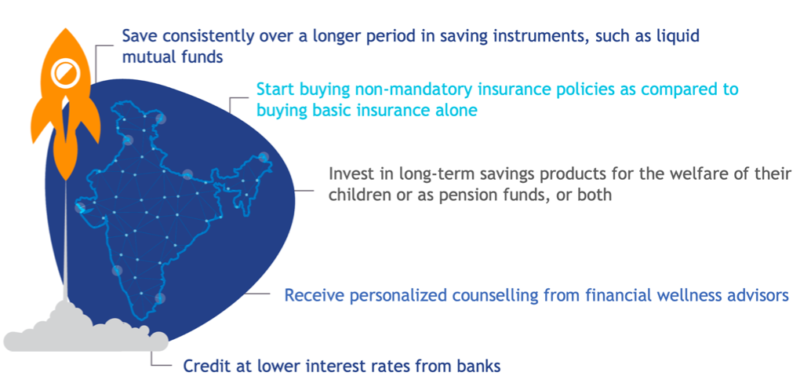

As mobile technologies and better information systems can bring more LMI segments into the realm of financial inclusion, we believe that India’s new wave of fintechs should start focusing more aggressively on building products and services that will empower these customers to take the following actions, as outlined in the infographic below.

We firmly believe that by engaging with fintechs and providing them with relevant inputs, we can create impactful solutions together to serve the financially excluded and build a better, less digitally divided society for the benefit of all.

This blog post is part of a series that covers promising FinTechs that are making a difference to underserved communities. These start-ups receive support from the Financial Inclusion Lab accelerator program. The Lab is a part of CIIE.CO’s Bharat Inclusion Initiative and is co-powered by MSC. #TechForAll, #BuildingForBharat

Anshul Saxena, and Sunil Bhat are senior managers at MSC, a NextBillion partner.

Anil Kumar Gupta is a partner at MSC .

Photo courtesy of MSC.

You May Also Be Interested In:

- Categories

- Finance, Technology