A Solution to the Drama of Digital Finance

Thank heaven I’m not an MFI manager.

Don’t get me wrong, managing a microfinance institution was probably the most rewarding thing I’ve ever done, but that was back in the ’90s, when my biggest tech problem was figuring out what sort of finance software to use. I was ordered to leave that decision to headquarters, which installed two different and expensive software systems, neither of which worked properly.

Now there’s digital finance.

Mobile banking.

Agent networks.

What’s a Luddite to do?

Because doing nothing is not an option, not when the competition is getting into the digital game. These new technologies enable MFIs to cost-effectively reach remote populations, opening up new market segments. Digital financial services (DFS) can also help to better manage the risk of fraud (though DFS has its own set of risks).

But once you’ve decided you absolutely must go digital, the next question is which business model to use. If setting up a financial software system was tough, choosing the correct digital model is multitudes more confusing.

But once you’ve decided you absolutely must go digital, the next question is which business model to use. If setting up a financial software system was tough, choosing the correct digital model is multitudes more confusing.

Should you develop your own digital platform or leverage someone else’s? Do you want to deploy your own network of agents? Will you enter into a partnership with a mobile network operator? Should you offer a DFS that another provider has developed and is also currently offering?

None of these are simple questions, dependent as they are on your MFI’s goals, environment and capabilities.

And then there’s cost. How does the model you’ve selected generate value for your MFI, and what’s the time frame for breakeven? Are you gaining value from direct services, from customer retention or from new customers? You’ll need to justify the proposed investment to your board, and the numbers aren’t small.

It’s easy for things to go wrong at this stage, to invest great sums of money and realize in the middle of your journey that you’ve picked the wrong model, or your projections are off.

Even if you’ve chosen wisely, it gets worse. There are a host of questions to answer at the implementation level. How do you implement your model? What types of skills will your staff need to implement and manage it? How will this new tech transform your organization? What are the key indicators to monitor and targets to set?

It’s exhausting.

But other MFIs and financial service providers (FSPs) have already taken this journey, and they’re sharing their experiences and decision trees in a series of digital finance toolkits. UNCDF’s MicroLead program team and PHB Development have just launched the first in a series of six practical toolkits sponsored by The MasterCard Foundation and titled, “How to Succeed in Your Digital Journey: A Series of Toolkits for Financial Service Providers.”

“We realized our partners needed to reduce the operational and transaction costs to reach deeper into rural areas,” said MicroLead program specialist Hermann Messan, “and for that they needed to go digital. Our MicroLead partners engaged in DFS at different levels and in different ways, and they all faced challenges. There were lots of sharing of experiences and perspectives and questions between our partners. So, we thought, why not collect their experiences and develop a more formal, structured approach for microfinance managers looking to go digital? We used MicroLead and PHB partners as the driving force in providing perspective for the toolkits, and this comes through both in the models and decision trees we defined as well as in the supporting case studies. This allowed us to structure the toolkits around FSP manager needs.”

Because mobile banking and digital finance cut its teeth in Africa, most of the toolkit examples and case studies come from that continent. However, the challenges that managers face in the digital arena are common across different markets.

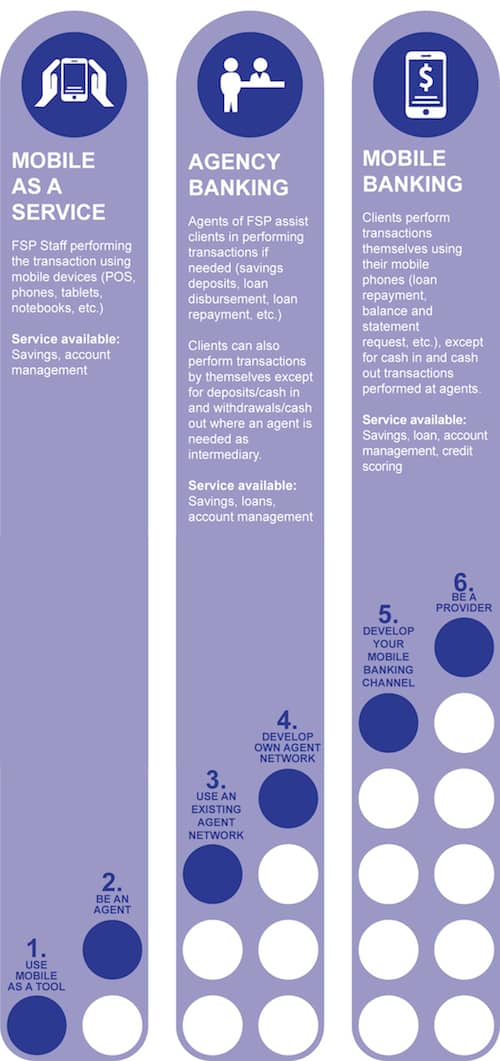

Toolkits are available in both French and English. You can download the first toolkit, “Use Mobile as a Tool,” and its associated case study here. Five more toolkits are on their way: “Be an Agent,” “Use an Existing Agent Network,” “Develop Own Agent Network,” “Develop Your Mobile Banking Channel” and “Be a Provider.”

“The toolkits give managers the opportunity to avoid mistakes that others have gone through,” says Hermann. “There is often a continuum from one model to the next, and what you choose will depend on your organization, its needs and the market.”

Kirsten Weiss is a communications consultant in San Mateo, Calif., who works as a writer for the UNCDF’s MicroLead program.

Photo: A Sinapi Aba client and customer service officer, Ghana. Courtesy of PHB Academy

You May Also Be Interested In:

- Categories

- Technology