Exploring Early Adopters of Mobile Money for Health: Database of innovators being compiled

Mobile money (payments through phones, usually via SMS) is rapidly becoming a powerful mechanism to extend financial services to the unbanked in low- and middle-income countries. There are more than 61 million mobile money users globally and financial transactions via phone are expected to rise from $12 billion in 2011 to $85 billion in 2016. In sub-Saharan Africa, more than 12 percent of the population without a formal bank account already uses mobile phones to conduct financial transactions.

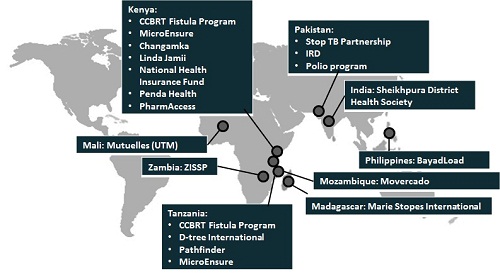

The Health Finance and Governance (HFG) project (which partners with my employer, Results for Development) is closely tracking the uptake of mobile money applications in health. HFG has identified 18 mobile money innovations that are being adopted by different types of programs (e.g. primary care, tuberculosis, maternal and child health) across public, private and non-state sectors in health. These programs are replacing cash payments with mobile payments to achieve the following benefits:

- Rapid, timely and reliable payments to individuals;

- Improved security in managing, sending and receiving payments;

- Improved efficiency and reduced administrative costs;

- Improved oversight and financial management, enhanced transparency and governance;

- Improved access to financial services, particularly in remote settings (requires cell phone connectivity).?

Early findings from HFG reveal that common uses of mobile money in health include:

- Payments for salaries, used in Zambia’s Integrated Systems Strengthening Program, and incentives for health workers, used in a StopTB Partnership program in Pakistan and for community health workers in Sheikhpura, Bihar;

- Collection of premium payments for health insurance schemes as employed by Mutuelles in Mali;

- Payments for providers, as used by Marie Stopes Madagascar, PharmAccess and Penda Health;

- Plus other applications, such as payments for health commodities, employed by Movercado, or health savings accounts as used by Changamka.

Several mobile money programs are highlighted here:

D-Tree International: Incentivizing patient referrals for obstetric emergencies

Since traditional birth attendants (TBAs) in Zanzibar are typically paid to assist deliveries at home, there is a financial disincentive for TBAs to refer patients to health facilities. D-Tree International established a mobile money system in Zanzibar, Tanzania, to incentivize timely and appropriate referrals for obstetric emergencies, allowing patients to receive access to care and any necessary follow-up. Payments are also sent to TBAs to cover costs incurred for emergency transportation when they accompany patients to health facilities. As of October 2013, more than 2,500 financial transactions had been sent to TBAs via mobile. According to D-Tree, the use of mobile payments has streamlined and improved overall management of payments to TBAs.

Mutuelles in Mali: Extending access

Health insurance Mutuelles in Mali face difficulties in collecting contributions from members in remote areas of the country. In early 2013, one of the largest organized associations for the Mutuelles, l’Union Technique de la Mutualité Malienne (UTM), designed and piloted a mobile money system to collect premiums for the Mutuelles. UTM launched this program in September 2013 and scaled it up to the national level. Mobile payments were adopted as the primary method for Mutuelle members to pay their contributions, and more than 102 members have used it to date.

Interestingly, UTM worked closely with the mobile network operator during the design phase of this program to ensure that it met the needs of Mutuelle members; they developed a payment system to collect contributions through small, incremental payments, and they also designed targeted SMS messages to educate them about mobile money.

Marie Stopes Madagascar: Reducing financial access barriers to care with mobile-enabled vouchers

In 2010, Marie Stopes Madagascar (MSM) launched a voucher program to subsidize care for family planning services, with a particular focus on reaching poor women in remote and hard-to-reach areas. MSM offers reproductive health vouchers to prospective clients through community-based delivery channels for around $10 U.S. Each voucher has a unique code and can be redeemed at one of 118 different health facilities in 12 regions of the country, in exchange for reproductive and contraceptive health care services. These vouchers enable women to receive family planning services for free. Providers submit the voucher codes and are reimbursed for their services electronically via mobile money. In addition to improving financial access to care for these patients, the use of mobile money has also helped MSM improve its management of the voucher program during the scale-up of this program.

Changamka Microhealth Limited: Enabling financial coverage with a health savings account

The lack of safe, cost-effective ways to save money over time makes it difficult for the poor to accumulate funds to pay for health expenses, even for expected medical costs such as maternity care. In Kenya, Changamka offers clients who may not have access to traditional banking platforms a mobile phone-based savings account to save money for outpatient or maternal health services. Changamka targets Kenya’s uninsured – nearly 90 percent of the population – and provides a convenient health savings account, particularly for the poor, near-poor and the informal sectors who also have difficulties paying for health care.

Learn more about mobile money here.

Are you a mobile money innovator?

If your organization works in health and is using mobile money, please complete the following survey to be included in the HFG Mobile Money database.

Are you considering using mobile money in your program?

Visit the HFG website or write to Marilyn Heymann (mheymann@r4d.org) for more information. You can also click here to subscribe to the HFG Mobile Money newsletter and receive regular project updates and additional information about mobile money in the health sector.

This blog originally appeared on the Center for Health Market Innovations website.

Marilyn Heymann is a program associate at the Results for Development Institute.

- Categories

- Health Care, Technology

- Tags

- product design