How Incorporating Behavioral Science into Cash Transfer Programs Is Changing Lives

Fighting poverty with direct cash payments is more common now than ever before. In 1997, only three developing countries had centrally managed cash transfer programs targeting poverty. Today, more than 120 do, and more than $200 million in cash is distributed daily. The adoption of cash transfers was a significant step in reducing extreme global poverty. Evidence shows that these programs work – both to reduce poverty and to boost human capital. For example, recipients spend the money on essentials like their children’s school supplies or investing in their small business.

Now there is more pressure on cash transfer programs to enhance their effectiveness. So how can we further help families make the best use of money?

Research from the emerging field of behavioral science—the study of how humans make decisions and take actions—suggests that light-touch design features may improve outcomes at little additional cost. The application of behavioral insights has already revolutionized the design of products, policies and programs with a diverse array of development goals. We can use these same insights to design cash transfer programs to set beneficiaries up for success.

Beyond giving people money, social assistance programs must help them be intentional with it. Behavioral science tells us that, regardless of income level, most people don’t think about how to spend an infusion of cash – be it a paycheck, cash transfer or anything else – right before receiving it. And as we know from studying behavior, in the case of cash transfers, that makes it less likely for the money to be funneled toward what people most want to use it for in the longer term, such as saving up to start a business. Fortunately, creating an easy avenue for cash transfer beneficiaries to set goals and make plans for achieving them can go a long way toward helping them make the most of their money.

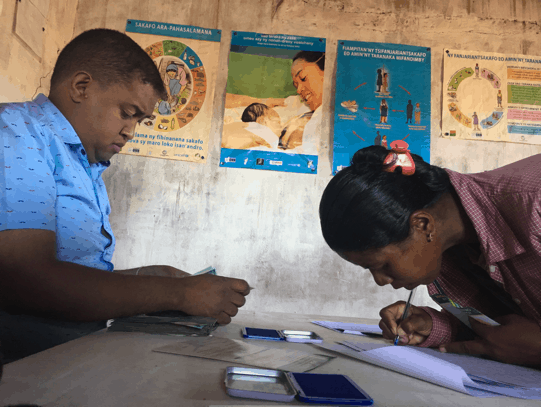

A cash transfer beneficiary in Madagascar receives a payment after selecting a savings goal.

Today, a new generation of cash transfer programs – currently being piloted in several countries in Africa – uses behavioral insights to help beneficiaries decide how to spend their cash and follow through on those plans. But the circumstances under which they receive the funds—like how long they have to wait on payment day or how close the local market is to the payment site—impact whether they put that intention into action. Other often-overlooked program design factors, such as the frequency of payments or how the purpose of the cash is framed, can disproportionately affect how people spend (or save) their money. Insights from behavioral science show that people act in predictable ways—and we can use that knowledge to design cash transfer programs that support people’s goals and continue to set them up for success.

For example, in our work, we have found that the way payments are made often caters more to administrators’ convenience than beneficiaries’ needs. But some innovators are already changing the timing, location and frequency of payments to suit recipients. For instance, GiveDirectly, a nonprofit that provides unconditional cash transfers, is experimenting with allowing beneficiaries in Kenya to choose when they’d prefer their payments to occur. This is important because getting money at the wrong time can actually increase stress. When cash arrives infrequently, it forces recipients to stretch funds until the next payment. But if it is transferred too often, recipients must save slowly over time, pulling their attention away from other critical tasks. While it isn’t always possible to pay everyone according to their ideal schedule, even offering some payment flexibility may help recipients achieve their goals more quickly.

A simple prompt for beneficiaries to consider how they’d like to use their money right before receiving it can also support their financial goals. Other tactics include reminders to follow through on plans, systems to provide feedback to people on their savings progress, and wallets to help them physically separate (and thus mentally separate) what they want to spend routinely from what they want to set aside for the future. Many inexpensive options exist that are fairly easy to put in place.

To bring more of these solutions to cash transfer programs, ideas42 and the World Bank, with financial support from the Global Innovation Fund, are launching a new initiative, Behavioral Design for Cash Transfer Programs. Working with government partners to identify the best options for incorporating behavioral designs in cash transfer programs across several African nations is a critical next step in improving this anti-poverty tool. We can then work to make behavioral science an automatic part of any social protection program that features a cash transfer.

Improving the efficiency of cash transfers can cut costs while maintaining and enhancing the collective agency of recipients. The next step in the evolution of cash transfer programs is to follow advances in other fields by providing low-cost, high-impact and effective support, based on behavioral research. We envision a social protection sector where all cash-based programming is designed to incorporate the latest findings from behavioral science research. With cash, families may imagine a better future; we should do all we can to help them take control of it.

Josh Martin is a vice president at ideas42, where he oversees behavioral science interventions in international governance and public service provision.

Laura Rawlings is a lead social protection specialist, where she oversees a number of research and program initiatives in the social protection field.

Photos by Dimitri Ralovason and Abi Warren, ideas42.

You May Also Be Interested In:

- Categories

- Finance, Technology