Serving the 57 Percent: That’s the percentage of American adults who are struggling financially – CFSI research illuminates their needs

At first, the headline number may seem hard to believe: 57 percent of American adults are struggling financially. But that’s what the Center for Financial Services Innovation (CFSI – a NextBillion Content Partner) found in its recent Consumer Financial Health Study. The research was conducted to understand the current state of financial health in America and to glean insights that can inform cross-sector efforts to improve consumer outcomes – and with a majority of the country affected, its value is clearly significant. CFSI recently released more data from its Consumer Financial Health Segment Profiles, breaking down the challenges and needs of different sub-groups within this 57 percent. We spoke via email with Aliza Gutman, the CFSI director who has led the study, about its findings – you can read the interview below.

James Militzer: Describe the study and why it’s significant; for instance, how does it differ from previous research on the financial needs of low-income populations in America, either in scope or focus?

Aliza Gutman: The Consumer Financial Health Study consists of a nationwide survey and consumer segmentation. We surveyed over 7,000 adults from across the United States and across the income spectrum, asking about financial behaviors, attitudes, preferences and product use. Consumers with annual incomes under $50,000 were over-sampled to provide a robust set of data on consumers in the lower half of the income distribution. However, since we aimed to understand the financial health of the entire country, we weighted the data back to the total U.S. population to report findings that are nationally representative.

As we developed the survey instrument, we consulted with industry experts and reviewed industry research and surveys. While some of these surveys focused on individuals’ financial well-being, others examined consumers’ use of financial products and services. CFSI’s Consumer Financial Health Study builds upon these surveys by including both of these elements.

The consumer financial health segmentation groups consumers based upon patterns of responses to a range of survey questions corresponding with subjective and objective indicators of financial health. The segmentation is, therefore, not a demographic segmentation; instead, it sheds light on the patterns among financial behaviors, attitudes and circumstances, and offers a new way of understanding consumers’ financial situations that goes beyond income, age, education or credit score.

JM: Could you briefly describe each of the consumer segments studied (or just the main segments) – their size, main characteristics/struggles and financial needs?

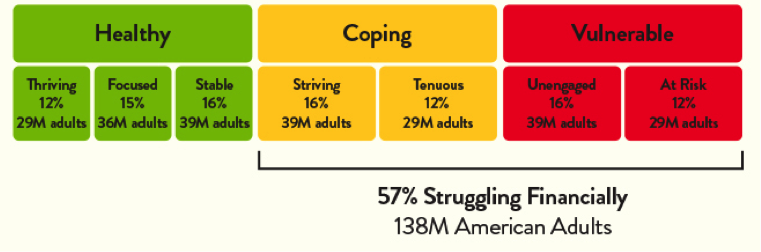

AG: The seven consumer segments derived from the segmentation analysis were grouped into three tiers: Healthy, Coping and Vulnerable, with the four segments in the Coping and Vulnerable tiers sometimes referred to in aggregate as the segments comprised of consumers who are struggling financially.

The three Healthy segments tend to do well across all indicators of financial health. Individuals in these segments are able to manage their day-to-day financial lives; they have a significant financial cushion in case of an emergency; and they are better positioned to seize financial opportunities. They also demonstrate the highest rates of checking account, savings account and credit card ownership of all segments.

The two Coping segments generally exhibit more moderate behaviors and attitudes across the financial health indicators, compared with their Healthy counterparts. These individuals are more likely to struggle with management of their day-to-day financial lives, to have less of a financial cushion for an emergency, and to be less well positioned to take advantage of financial opportunities. Individuals in these segments tend to use a variety of financial products and services – traditional, non-bank and new technology-enabled – to manage their financial lives. These two segments are most strongly differentiated by their propensity for day-to-day planning; all members of the Striving segment, for example, plan ahead for large irregular expenses, and they have the highest rate of budgeting. In contrast, no one in the Tenuous segment plans ahead for large irregular expenses, and they have a fairly low rate of budgeting.

The two Vulnerable segments are doing the least well across financial health indicators. These individuals are more likely to be struggling with their day-to-day financial lives; they have little or no financial cushion in case of an emergency; and they are not prepared to seize financial opportunities for security and mobility. They are the least likely of all segments to own a credit card and the most likely to be unbanked. The Unengaged segment differs significantly from other segments due to the frequency with which they answer “don’t know” to survey questions. Of all segments, the At Risk segment has the most precarious financial situation; more than a quarter say they could only make ends meet for a week or less if they were to experience a sudden drop in income.

JM: Was there anything you found particularly surprising, alarming or hopeful about the research findings?

AG: Surprising:

- When we started, we had several hypotheses about what the outcome of the segmentation analysis might be. Perhaps one segment would excel in day-to-day financial management with little preparation for financial shocks or opportunity; while another segment would be equipped to deal with unforeseen expenses, but would not plan or save for the future; while another segment would excel in all three core elements of financial health. Another possibility was that some segments would excel in certain indicators (like keeping up with bills), while exhibiting less healthy behaviors in other indicators (such as debt management). However, we found that that indicators across the core elements of financial health generally trend together (high, medium or low), highlighting the degree to which the components of financial health are intimately connected to one another.

- We also found that more than one-third of households (35 percent) that are struggling financially are also part of the wealthiest half of America (make more than $60,000 annually).

Alarming:

- More than a fifth of the population (22 percent) does not know how long their household could make ends meet if faced with unemployment, a longer-term illness, job loss, economic downturn or other emergency that caused a drop in income.

Hopeful:

- People of all income levels are financially healthy. More than one-third of financially healthy households (35 percent) make less than $60,000 annually.

JM: What are the main takeaways from the research for financial services providers? How would you like these findings to inform future product development or outreach to these communities?

AG: 1) Fifty-seven percent of American adults – approximately 138 million – are struggling financially. This proportion is larger than the population categorized as “unbanked” or “underbanked,” which underscores how widespread the consumer challenges and business opportunities are. Investing in consumer financial health represents an immense opportunity for financial services providers to address unmet needs in the market, gain loyal customers and build long-term revenue streams.

AG: 1) Fifty-seven percent of American adults – approximately 138 million – are struggling financially. This proportion is larger than the population categorized as “unbanked” or “underbanked,” which underscores how widespread the consumer challenges and business opportunities are. Investing in consumer financial health represents an immense opportunity for financial services providers to address unmet needs in the market, gain loyal customers and build long-term revenue streams.

(Left: Aliza Gutman)

2) The data from the study suggests that financial health can be improved with the adoption of beneficial financial habits, even if income remains unchanged. Financial products and services that enable individuals to cultivate these behaviors – particularly those related to planning ahead and saving – can be instrumental in helping households achieve financial health. The financially healthiest Americans plan ahead for large, irregular expenses and maintain regular savings habits. Understanding what challenges people face and what behaviors are key contributors to financial health is essential for creating better products that help Americans improve their financial situation.

3) The fact that so many struggle with financial health in spite of the abundance of financial products indicates there is a gap in the market: an insufficient supply of high-quality products designed to improve financial health. For example, 74 percent of consumers say they own a savings account, yet more than half of them (52 percent) do not have a planned saving habit, 20 percent of them have less than $1,000 in non-retirement savings, and 42 percent of them lack confidence in their ability to meet their short-term savings goals. Additionally, less than half of American adults (45 percent) are confident they can achieve their long-term goals for becoming financially secure. We know consumers are loyal to those who meet their needs and treat them well; 63 percent say once they find a product or service they like, they tend to be very loyal and don’t like to switch. Hence, there is a significant opportunity for financial services providers to develop and market products that help consumers adopt and sustain behaviors that contribute to improved financial health.

JM: How will these findings affect CFSI’s work going forward?

AG: We have spent much of this year analyzing the data from the Consumer Financial Health Study and releasing insights to help the financial services community understand the findings. CFSI will build upon this foundational body of knowledge in the coming years by developing financial health metrics, testing products’ impact on financial health and examining the connection between improved financial health and business model drivers. We are currently developing tools to help providers better measure consumer financial health and working with them to help embed these practices into their procedures and cultural norms.

Reports and resources from the Consumer Financial Health Study can be downloaded from CFSI’s website:

JM: Does this study point toward a need for deeper research into any particular aspect of the financial needs of low-income Americans – and if so, what additional topics should be the focus?

AG: We find that for as many insights that are gained with a particular piece of research, there are always more questions raised. We highlighted a number of these questions in the segment briefs to give providers a starting point to think about their own customer research and approaches to product development and measurement. For example:

- Do consumers in the Striving segment have planning tools that meet their needs and help them make decisions efficiently and effectively? If not, what are they currently doing, what are their challenges and what improvements do they most desire?

- What are the most effective strategies to help the Tenuous segment plan ahead? More than half (57 percent) say they would plan ahead if they could. What is preventing them from planning, and what tools and motivators can help them reap the benefits of thinking and planning ahead financially?

- What is driving the lack of awareness or engagement amongst the Unengaged segment? Do they not wish to engage, or have they not identified products that meet their needs? Can smart design of default settings help individuals in this segment get the most out of products and services without having to engage deeply or proactively?

- What type of account design will help At Risk consumers avoid the pitfalls that previously led them to close accounts (or have providers close them) while also providing the convenience and functionality they need? What types of guardrails and features promote consumer success and mitigate provider risk?

James Militzer is the editor of NextBillion Financial Innovation.

- Categories

- Education