A Mixed Bag in Kenya: Safaricom’s products have moved far beyond M-PESA – but are they reaching the poor?

First the good news: With transaction amounts equivalent to over 40 percent of Kenya’s GDP flowing through M-PESA, Safaricom’s success in person-to-person mobile money transfers is the stuff of legend. And over the last two years, the telco and its partners have been adding innovative, value-added financial services (those beyond basic P2P transfers) to the M-PESA product. A recent nationally representative survey conducted by InterMedia found that 10 percent of Kenyan adults (ages 15+), or 13 percent of mobile money users, have used M-Shwari – a mobile savings and credit product offered by Safaricom in partnership with Commercial Bank of Africa. This makes it Kenya’s most widely used value-added mobile money service. The figures mirror Safaricom’s recently published supply-side total of 2.4 million active M-Shwari users.

InterMedia’s Financial Inclusion Insights survey in Kenya also found that Lipa na M-PESA, a merchant payment tool, is the second most common value-added mobile money service, used by 3 percent of Kenyan adults. This figure includes both merchants and customers who said they had used the product. Smaller percentages of Kenyans reported using other value-added products and services recently introduced to the market, such as M-Kesho, a bank-linked savings account; Lipa Karo na M-PESA, a payment service for school fees; and M-Kopa, a mobile money-based product for acquiring solar electric systems.

Value-added mobile money services have the potential to bring great benefit to consumers, particularly those with less access to traditional financial services. Savings tools like M-Shwari can help the poor put money aside so they can better deal with negative financial shocks when they happen, such as a household member’s illness. Lipa na M-PESA provides a safe way to make payments at shops, allowing rural residents to purchase goods without having to carry cash over potentially long distances. Similarly, Lipa Karo na M-PESA provides a safe way for rural residents to pay school fees without having to travel with cash, particularly helpful if their children attend school in urban areas.

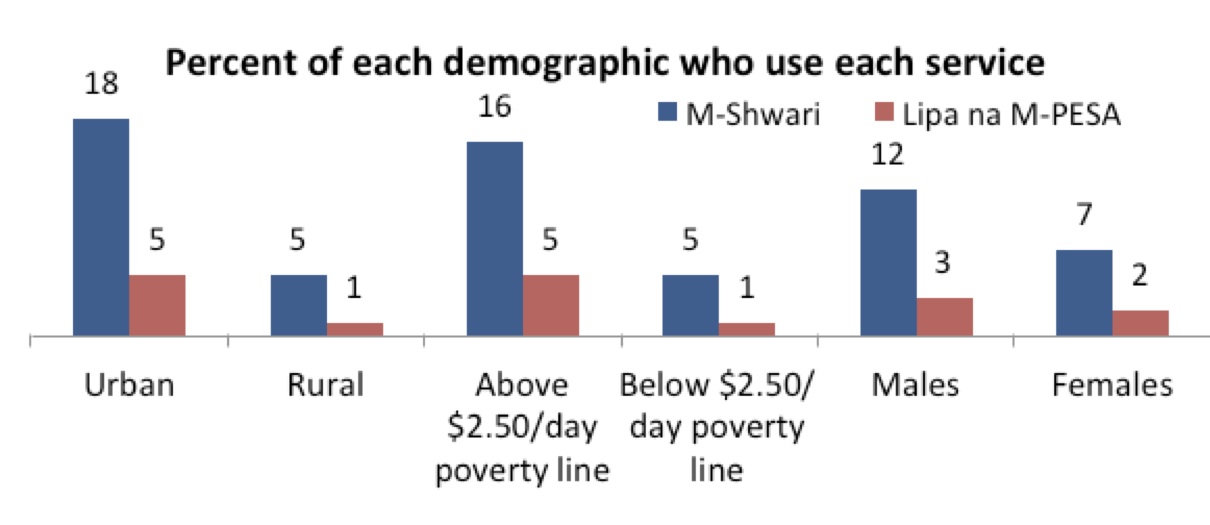

So what’s the problem? Looking into who is using these services, we found that the groups that may benefit the most from them are currently the least likely to use them. Relatively fewer rural residents, those below the poverty line, and females use M-Shwari and Lipa na M-PESA than do their urban, above the poverty line and male counterparts. And increasing uptake among these groups has proven to be a challenge, even when they’re already M-PESA users.

Individuals who already use mobile money but don’t yet use the additional services – a group that includes many poor, rural and female Kenyans – are a prime audience. Yet among active mobile money users below the poverty line, only 13 percent have used any kind of value-added mobile money service, compared with 26 percent of active mobile money users above the poverty line.

Individuals who already use mobile money but don’t yet use the additional services – a group that includes many poor, rural and female Kenyans – are a prime audience. Yet among active mobile money users below the poverty line, only 13 percent have used any kind of value-added mobile money service, compared with 26 percent of active mobile money users above the poverty line.

Better understanding the needs of underrepresented groups may enable greater uptake. InterMedia is undertaking a number of targeted studies to identify the barriers that hinder uptake among these groups, as well as the motives of early adopters of the services, in order to understand what factors may lead to growth. As we conduct follow-up studies, the Financial Inclusion Insights program will continue to provide stakeholders with information they can use to shape the future of digital financial services, particularly among underrepresented populations.

- Categories

- Education