Lessons Learned Using Mobile Tools to Compile Financial Diary Data

Editor’s note: Throughout 2017, NextBillion is organizing content around a monthly theme, dedicating special attention to a specific sector alongside our broader coverage. This post is part of our focus on financial inclusion for the month of June.

In 2015, Catholic Relief Services (CRS) sent smartphone-toting field data collectors to seven villages around the town of Kasama, in Zambia’s Northern Province, to help answer an important question: Could CRS’ local savings and lending group model expand financial inclusion and improve resilience for vulnerable households?

Using digital financial diaries on each mobile device to record the financial behavior of 272 households, through more than 200,000 cash, barter, in-kind and financial transactions, CRS got its answer in preliminary study findings. Its Savings and Internal Lending Communities (SILC) doubled the rate of large business and household purchases for all SILC members with funds from loans, savings dividends and small, frequent savings deposits. The most significant increases were in the payment of school fees and household asset purchases.

Financial diary methodology proved to be a powerful tool for studying financial inclusion in Zambia, but practitioners of this highly detailed and time-consuming monitoring and evaluation technique would not have reached their desired research breadth and depth had they not completely switched from paper-based to digital tools about 40 weeks into the more than two-year data collection and analysis effort.

Using a mobile data collection and analysis app (which also worked offline) and a cloud-hosted database, CRS drew household data from rural areas in real time – even when connectivity was spotty – and accurately amassed thousands of data points generated by tracking people’s financial lives each week. At the same time, a CRM tool built into the app increased the productivity of field teams collecting this data by allowing CRS to set goals for each survey agent and track progress against those goals.

Financial Diary Methodology. Source: Bankable Frontier Associates

Digital Tools Provide Quality Check On Massive Data Flows

CRS research officer Samuel Beecher, who managed the work, said mobile tools helped ensure data quality for a key component of financial diary research:

“One often-overlooked part of financial diaries data collection and data quality is balance checks: making sure that weekly inflows and outflows sum to the same number. … It is common for weekly inflows and outflows not to match at first glance as the respondent may intentionally or unintentionally leave out all of the transactions.

“After switching to mobile technology it was much easier for the imbalances to be identified in a timely manner and for the enumerator to visit the household soon after the initial interview to probe about their transactions and correct the data.”

First tested in Bangladesh in 2000, financial diaries were popularized in 2009 with the publishing of “Portfolios of the Poor.” Financial diary-based research has “changed the financial inclusion and microfinance sector by revealing that the poor are adept money managers leading complex financial lives,” wrote research funders from the MasterCard Foundation, which provided financial support to the CRS effort, combined with research help from Microfinance Opportunities. Financial diaries have gauged the financial strains facing smallholder farmers in Mozambique, Pakistan and Tanzania as well as the poor in Kenya and Mexico. Financial diaries were recently used in the U.S. Financial Diaries project to uncover the income volatility that has unsettled many U.S. households since the 2008 recession.

When they each began their individual financial diary projects, both U.S. Financial Diaries and CRS researchers headed down the paper path only to switch gears once they found software that could digitize their work. In CRS’ case, the solution came from TaroWorks, our mobile data collection and analysis app, which is also an offline CRM and field force management platform, powered by Salesforce.

Beecher knew that using financial diaries in Zambia could provide insight into household financial behavior but recognized the obstacles presented by paper data collection:

“The panel nature of the (financial diaries) survey allows for more accurate measurement of the frequency and magnitude of different transaction types because of the number of interviews conducted. The longitudinal nature of the study allows for the analysis of trends, and the detailed nature of the data allows for in-depth case studies of individual households.

“The data collection process at the start of the project relied on paper data-entry sheets that a team of three full-time data clerks entered into an Access database. … The project decreased 24 working hours each week by having the enumerators enter the data directly into the database via the phone, not to mention the time enumerators saved conducting the surveys by entering the data on the phone compared to writing it on a paper questionnaire.”

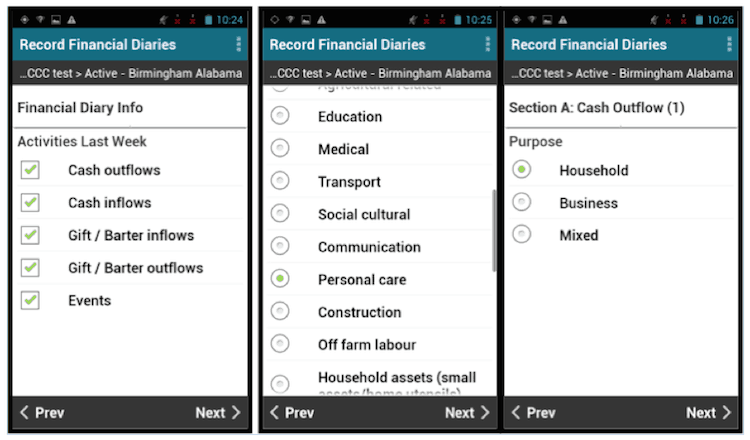

Financial diary mobile survey using TaroWorks. Source: Catholic Relief Services

Financial Diary Use Expands To U.S.

The U.S. Financial Diaries team’s data collection task was equally daunting, according to their recounting of survey methodology.

“The volume of information gathered during the interviews could be large – on average, field researchers recorded 56 separate cash flows in an interview (cash flows are defined as the movement of money into or out of a household, or between financial instruments).

“The study was designed with mechanisms to mitigate the burden of collecting such detailed data. One such mechanism was that each diary questionnaire would inform the next so that subsequent questionnaires would eliminate redundant information and be automatically adjusted for new or different information. However, because of the demands on field researchers and the challenges described above, data entry sometimes lagged data gathering. … The hiring of additional data entry staff and our transition to having fieldworkers enter data in real time using tablets mitigated this challenge over time.”

Timothy Ogden, who oversaw the U.S. Financial Diaries project as managing director of the Financial Access Initiative, told the publication Next City that earlier methods of collecting data on financial lives didn’t provide enough detail and substituted direct observation with fuzzy recollection.

“Most of previous research on financial lives was based on phone surveys, one time, try to get people to recall over a whole year, their financial lives,” Ogden said. (Read more.)

In contrast, CRS enumerators moved to each research village when the project began and lived among the survey households for the entire study period, becoming a part of the community and developing a level of trust with the study subjects, which allowed them to dive deeply into each household’s earning, spending and savings patterns.

Fintech for Financial Diaries: Lessons Learned

Beecher believes there are other advantages to using a mobile data collection and analysis application and offline CRM to gather and analyze financial diary data – beyond the ability to handle large data sets, as was the case in Zambia where more than 55,000 financial diaries were created across 272 households.

- Increased productivity: It’s one thing to provide mobile tools for collecting field data but another to ensure that the data collectors are where they need to be, when they need to be, doing what they’re tasked to do. Study logistics were made even harder by the fact that “respondents in the Northern Province of Zambia live a transient lifestyle, with seasonal migrations to neighboring villages for fishing, agriculture and yearly harvests of various non-wood forest products,” said Beecher. Using TaroWorks’ field force management CRM capability, as each completed survey and household visit was uploaded to the cloud database, it registered on a dashboard visible to field agents and their managers (even when mobile or internet service wasn’t available) so progress toward their data collection goals could be measured and targets adjusted as needed.

- Improved data quality: Data validation checks already programmed into the diary questionnaires reduced input errors by preventing typos or other data anomalies. Given TaroWorks’ ability to collect data offline when in rural areas and save the information for upload to the database when within range of connectivity, Beecher reported practically no data was lost over the course of the two-year collection effort.

- Reduced cost: Digitizing the financial diaries process eliminated the need and related expense of having data entry clerks transfer that information from paper to a database system.

Among the obstacles overcome and lessons learned by Beecher and his CRS colleagues using mobile technology to enhance and scale financial diary collection:

- Prepare for problems with mobile devices: Living in villages without electricity, field data collectors were given solar-powered battery chargers to keep their mobile phones up and running. But as Beecher explained: “Running the application and entering data throughout the day used a lot of battery and there were cases (especially during the rainy season) where solar chargers did not work optimally. The high rate of use and having the batteries drain frequently led to a short battery life.” Unfortunately, spare batteries and replacement parts for the mobile phones, which were purchased outside of the country, were not available within Zambia. Here are tips to help reduce difficulties with mobile devices used in harsh field conditions.

- Develop a robust software and hardware training program: The project reinforced the importance of rigorously training team members not only on the use of the mobile app but also the mobile device employed to administer the survey. Beecher concluded: “The enumerators hired by CRS had backgrounds in development studies and the social sciences and received a number of hours in training on the smartphone and TaroWorks application, so digital skills and competency was not an issue. (Nevertheless) introduction training is only the beginning and refreshers are essential, so organizations should factor this into their timelines and budgets. In these trainings, demonstrate how mobile technology can make the enumerators’ work more efficient and share with them how marketable of a skill it is to be expert in mobile technology.”

Elaine Chang is senior manager, global market development for TaroWorks.

Top photo, a customer using TaroWorks in Kenya.

Small photo of CRS financial diaries interview courtesy of Henry Tenenbaum, 2016/Catholic Relief Services

You May Also Be Interested In:

- Categories

- Finance, Technology

- Tags

- data, financial inclusion, fintech, research