One Village at a Time: A Women-Led Model for Bringing Digital Services and Financial Inclusion to Rural Bangladesh

Women customers constitute a huge market in Bangladesh’s rural economy, where many men have migrated to cities or foreign lands in search of work, leaving their wives and female family members behind to manage their households and care for their families. As a result, these women are increasingly shouldering more responsibilities, making financial decisions and participating in the local economy. Yet these new responsibilities have required them to interact with government agencies, banks and other service providers to obtain vital services traditionally handled by men — and many Bangladeshi women have struggled to orient themselves in this new reality.

In response to this need, Zaytoon Business Solutions — a Bangladeshi financial services company — is working to give women and other underserved rural people access to technology-based financial and government services by establishing village digital booths (VDBs) in every village across the nation. Its mission is to increase access to formal banking services in rural areas by acting as a mediator between rural unbanked customers and the banks, microfinance institutions, mobile financial services and insurance providers that hope to reach them. Zaytoon also collaborates with government utility agencies and educational institutes to facilitate payment of electricity, gas and water bills, and educational fees — as well as government services and safety net payments — through the VDBs. These booths — staffed by both men and women who run them as small businesses — help advance the company’s mission by providing services that range from withdrawing remittances and making online deposits, e-commerce purchases and other financial transactions, to obtaining telemedicine services, applying for birth registration, passports and national identity cards, and paying land taxes. These services have traditionally been time-consuming and difficult, but VDBs staffed by knowledgeable local agents have made them far easier to navigate, while providing customers with the convenience and comfort of accessing them closer to their residence.

VDBs are an extension of Zaytoon’s existing agent model, which it operates in partnership with banks to bring financial services to rural populations. While its agency banking network focuses only on financial services, VDBs operate at a village level and focus on bringing both financial and government services to rural people — while offering women in these communities a valuable entrepreneurship opportunity that can provide them with a source of income.

Through its ground-level operations, Zaytoon observed that these rural women are willing to work, but they lack opportunity. Identifying this gap, the company piloted a women-focused program to train them as VDB entrepreneurs. The initiative has provided rural women with a chance to engage in income-generating activities outside their homes, boosting their participation in the local economy and improving their social standing within the community. Though the number of women-owned VDBs is still small, this model is showing promising potential to scale.

Below, I will discuss this unique approach to the last-mile distribution of essential services, exploring how Zaytoon has leveraged it for the benefit of both customers and the women entrepreneurs who serve them.

A Pathway to Entrepreneurship for Bangladeshi Women

Meet Tazkia Chowdhury, the first woman entrepreneur to own a VDB. She lives in Teghoria — a small village in Bangladesh’s Munshiganj District. Fueled by the desire to stand on her own feet, Tazkia started her entrepreneurial journey in March of 2023. However, her road to entrepreneurship was not easy. Pre-existing gender norms and deeply entrenched beliefs about women’s role in society were major entry barriers. In addition to restrictive norms that discouraged women from working outside their homes, Tazkia faced challenges in raising enough financial capital from formal avenues to launch and run the business. To start a VDB, an entrepreneur requires 50,000 – 60,000 Bangladeshi taka (around US $418 – $502) as a fixed investment, along with 300,000 taka (around $2,510) for liquidity to enable daily transactions. For rural Bangladeshi women, this represents a huge amount — particularly since most of a household’s income is earned by its male members, while women typically have very little savings.

In Tazkia’s case, she was able to mobilize the necessary funds with support from her husband, which allowed her to cover the initial startup and liquidity costs. Zaytoon assisted her in securing a Point of Sale (POS) machine through its partner bank, which enabled her to facilitate customer transactions, and also paid for branding and other fixed costs like office furniture. Going forward, the company plans to provide POS machines and QR code generators directly to its agents. Zaytoon’s smooth recruitment and onboarding process offered Tazkia various types of training, teaching her to oversee business operations, understand the product suite VDBs offer, manage financial transactions, troubleshoot technical issues, and provide customer service and documentation. It also provided her with digital literacy training, equipping her with the skills and knowledge she would need to run the VDB successfully. After a few months of training, she started operations in June of 2023.

After starting with a modest footfall of just 240 customers in the first month of her business, Tazkia’s booth quickly grew — she served around 4,800 customers from July 2023 to April 2024. She has sold 20+ financial and non-financial products to her customers, and the demand is growing every day. The main drivers of her revenue include financial/banking services like account opening, cash-in/cash-out, remittance and POS/QR transactions, along with the online payment of land-related taxes — in addition to government applications, utility bill collections, e-commerce, telemedicine and insurance services, and e-ticketing, among other services.

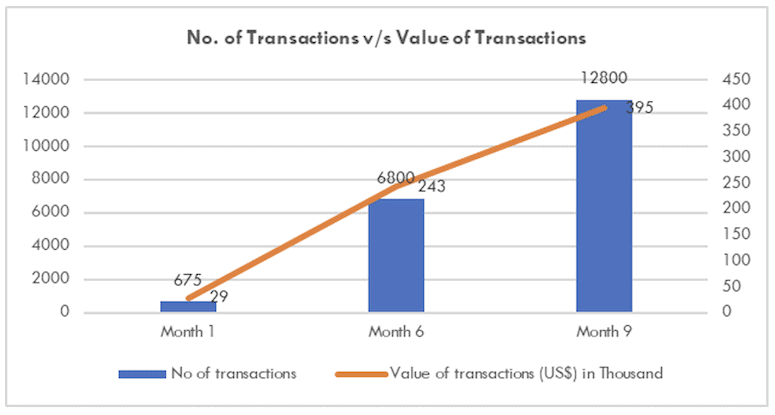

VDB entrepreneurs earn revenue on a commission basis by providing all the above-mentioned services and products. During this period, Tazkia carried out 12,000+ transactions with an aggregate value of US $395,000 (Figure 1). From July 2023 to April 2024, her monthly income grew by an impressive 1,085%.

Figure 1: Monthly Growth in Transaction Volume and Value

Tazkia’s story is not an outlier. Based on the positive response to her business, Zaytoon replicated this model in other operating districts from October 2023 to January 2024, supporting five more women in starting their own VDB businesses. Today, all of these six women agents are proud members of Zaytoon’s agent network, with the confidence to break their social shackles and run their businesses independently. And these women-owned digital booths — located in Vararia, Telkupy and Baultali — are recording a gradual increase in their number of women customers and volume of transactions, as these customers often have a preference for women-owned/women-managed VDBs. Women agents are familiar faces in the rural communities they serve, making it easier for women customers to visit them and seek their assistance for their various needs. In turn, these agents can meet the demands of their communities, while earning a good commission on the transactions conducted and the products sold at their outlets.

This trend is reflected in Zaytoon’s sales figures, which clearly show that women-owned VDBs perform better than their male-owned counterparts in its portfolio of 250 VDBs. Though most of these VDBs are run by men, this handful of women-owned VDBs are showing promising results. Within a short span, the company’s women-owned VDBs have served a large number of women customers across various product suites. So far about 7,600 women customers have accessed a variety of essential services from these women agents since their start of business operations.

Expanding Access to Services Beyond Finance

VDBs’ digital-first approach starts with financial services, but the booths have built upon that value proposition by also offering health services and social benefits under the same roof.

For instance, Zaytoon uses EkPay — an aggregator platform — to deliver financial and e-services from VDBs. In partnership with Soowgood Healthcare, it facilitates video consultation with doctors and arranges delivery of medicines at VDBs, making healthcare services accessible for rural customers. Zaytoon’s other prominent partners include a2i, Mutual Trust Bank, BRAC Bank, City Bank, TAP MFS and Upay MFS, among others.

Working as a service aggregator, Zaytoon is building a seamless platform for rural customers to access quality services conveniently in an affordable manner closer to their homes.

For example, the usage of telemedicine has been a particular area of growth in the VDBs operated by women. Sabina Akter, a customer of the Teghoria VDB, sums up its value: “I feel happy and privileged as I can avail healthcare advice from specialist doctors at a low cost near my home at this VDB. Now I avoid traveling 50 to 60 kilometers to healthcare centers in Dhaka, which costs extra and takes all day. There is no hassle of making online and offline appointments, which is necessary if I travel to Dhaka.”

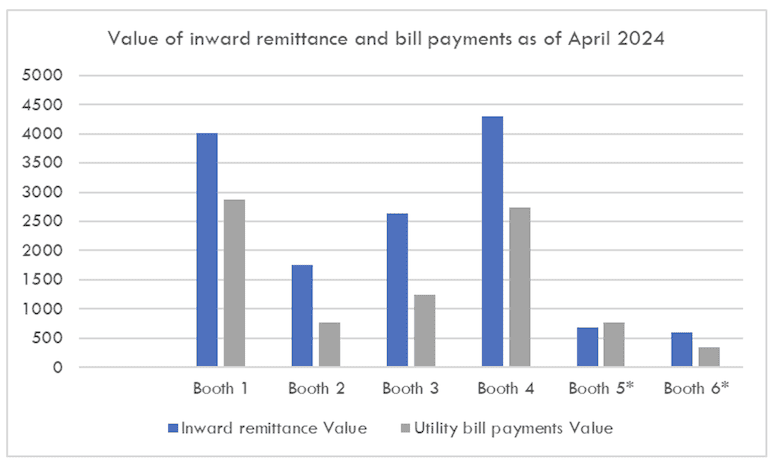

Other VDB services that are gaining traction include school fee payment, the purchase of household appliances, financial account opening and online shopping. Remittances and utility payments also remain in demand: As of April 2024, these booths had conducted inward remittances cumulatively valued at US $13,996, and utility bill payments valued at US $8,725 (Figure 2).

Figure 2: Trends in Inward Remittance and Bill Payments Transactions at Women VDBs. Note: Booth 5 and 6 started operations in March 2024, later than the other VDBs

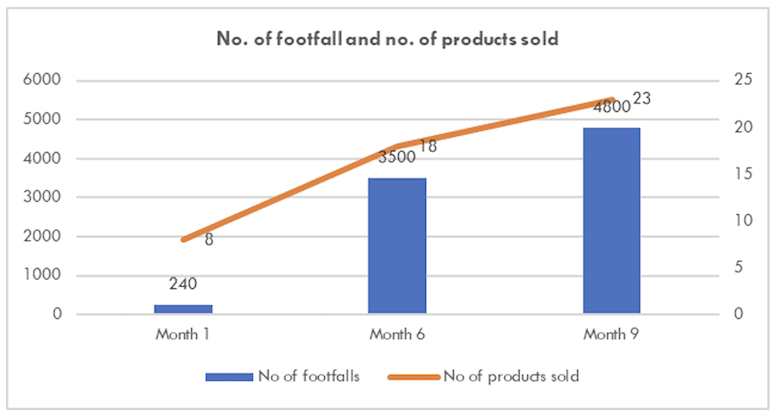

The convenience of accessing a bundle of affordable financial and non-financial services — along with the comfort, trust and familiarity of receiving these services from local women — are some of the crucial factors propelling the growth of footfalls of women customers at these booths (Figure 3).

Figure 3: Growth in Customer Footfall and Number of Products Sold at a VDB

Encouraged by this growth trend, the company aims to increase the footprints of women-led VDBs in other districts, with the ultimate goal of bringing this one-stop-shop platform to every village in the country. In doing so, it demonstrates the business case for investing in women agents, whose work brings them not only income and financial independence but also social recognition and renewed confidence in their ability to manage their businesses and households on their own.

Zaytoon’s mission is to ensure that 20% of its financial kiosks are owned by women in the forthcoming years. Through this model, it hopes to usher in a wave of social change, driving women’s economic empowerment while bringing essential services to low-income communities. With support from the government and development agencies, this digital-first approach could help pave the way for a smart and cashless Bangladesh, where every citizen becomes comfortable using digital banking and other services, one village at a time.

Garima Singh leads the communications and business development verticals at FinValue Advisors.

Photo: Tazkia Chowdhury with a woman customer at her booth. Credit: Zaytoon

You May Also Be Interested In:

- Categories

- Finance