De-Mythifying Financial Education

Somewhere in the hinterlands of the state of Odisha, with support from a respected local NGO and a public sector bank, a rural couple opened a bank account under the government of India’s ambitious financial inclusion agenda. They were trained on the basics of banking through the agent in their village, and looked forward to using their prized bank account. They had wide-eyed expectations about realising their dreams by using the new facilities. Unfortunately, these high hopes were rapidly buried as the agent withdrew his services not long after the end of the training programme. The disheartened couple gradually forgot the training lessons.

Proponents of financial education (FE) programmes feel that the population at the base of the pyramid lacks the acumen to manage its finances. Formal financial services providers (FSPs) are consequently often given a key role in building this know-how as they market their products and provide training to use them. A variety of other agencies, including government departments, third-party agent aggregators, NGOs, etc., join in to augment the efforts of FSPs.

Financial education, it is argued, endows the customer with practical skills to understand, access and more effectively use complex financial services. But these implementation partners face immense challenges: agent motivation, customer expectations, logistical hurdles, the political economy, etc. It is difficult to walk the rustic roads and bring comprehensive and sustainable financial capability to the BoP.

Part of the trouble lies, curiously, in the series of myths that inform the FE programme designs.

There is still a prevalent myth that the BoP lacks financial management capabilities and needs to be “taught” how to save and budget. This is as misguided as it is patronising. The poor have highly sophisticated mental accounting models to plan their finances. (MicroSave’s MetaMon Research project helped us decipher people’s money management principles in their own language and extract the common metaphors that they associate with them.) The poor manage their cash flows so ingeniously that despite scarce and unpredictable financial stocks and flows, they are able to take care of expenses.

Like many of us, the poor are rational decision makers and use both saving up and saving down to manage their household cash flows. MicroSave is privileged to have been able to study and learn the extraordinary, varied and creative ways poor people use to save from their meagre earnings, and the mental models that underpin them. During our extensive research on financial product uptake in eastern Uttar Pradesh in India, we explored the decision-making processes of the poor. We discovered that they rely not only on their own experience as well as information provided by the FSP, but also – and most importantly for their final decision – gather the experience and recommendations from opinion leaders in their community. Poor customers assess any financial product on offer with this knowledge base; small wonder, then, that we invariably find more than half of product uptake is driven by word of mouth.

There is often misguided belief that after financial training programmes, the poor will be empowered to seek out and use financial services available in the market. This assumes that the poor have access to these services. However, as the Odisha case depicts, lack of access to agents erased all the financial capability of the hapless couple. In one of MicroSave’s earliest path-breaking investigations into the savings culture in Uganda, we saw the common thread of “easy to access and easy to understand” running through all the systems adopted by the poor. More recently, the project “Safe and Smart Savings Products for Vulnerable Adolescent Girls in Kenya and Uganda” amply demonstrates that a training and mentorship FE programme, so long as it is accompanied by access to an individual savings account, was instrumental in improving savings behaviour (amount and frequency) among young females living precarious lives in urban slums. (See MicroSave Briefing Notes 112, 117 and 118 to learn more about this programme.) The availability of financial services and the ability of the poor to access and experiment with them is the key to converting financial education into the intended financial capability.

Courtesy of MicroSave

In the schools we observed, the education paradigms are based on curriculums. But this approach might not be the best when we aim to build capabilities of people to take sound financial decisions. In Briefing Note 112, Wright et al. discuss that product-based, experiential financial education as part of a well-designed product marketing strategy is likely to be the way ahead for delivering financial education on a sustainable basis. Fischer et al. found that during financial education training simple, direct, and actionable points have larger impact than sharing theoretical concepts. People learn best by doing. In experiential learning one makes discoveries and experiments with knowledge firsthand. According to David A. Kolb, an American educational theorist, knowledge is continuously gained through both personal and environmental experiences.

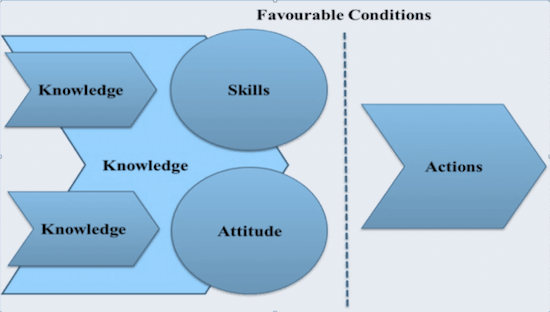

Based on our extensive research, we have come out with a framework for those planning FE interventions. We argue that knowledge created by a variety of information sources influences skills and attitudes of the individual, which then leads to practice/action in the form of financial decision. Skill and attitude development is not necessarily a linear and complementary process – one doesn’t generate the other. For example, a same savings product when introduced by a friend will have more salience for an individual than when offered by an FSP agent. FE is complex, as it is deeply influenced by the contextual environment in which the client is embedded.

Four key lessons should be at the forefront of an FE design:

- Poor people understand how to manage their money and have clear mental models for doing so – ignore these at your peril!

- Lack of knowledge is not usually the reason for poor uptake and usage – look to improve product design, delivery channels and marketing/communication (including through community opinion leaders).

- Look beyond traditional curriculum design to incorporate experiential learning.

- Understand the interplay between knowledge, skills, attitudes and actions … well leveraged, they can lead to regular “practice” and use of products/services.

To contact MicroSave, email Research@MicroSave.net.

Graham Wright founded MicroSave and is currently its group managing director; Akhand Jyoti Tiwari is a senior manager who leads behavioural research and design work at MicroSave; and Nitish Narain is a manager in inclusive finance and banking at MicroSave.

Photos courtesy of MicroSave

You May Also Be Interested In:

- Categories

- Education