Four Ways Digital Finance Can Prepare for the Next Wave of Mobile Money Disruption

Banks and telecoms in the developing world have pioneered financial systems that operate over mobile phone networks, which now have more than 118 million active accounts (30-day basis). It is an industry that prides itself on innovation and moving at the high speed of technology.

However, banks and telecoms are often some of the largest companies in their respective markets, limiting their agility and ability to take some of the risks associated with innovation. Further, banks are primarily structured to manage their risk, and telecoms are designed for sales and distribution. Neither banks nor telecoms invest heavily in the research and design required for innovation or employ many engineers who develop technology.

While there has been an impressive proliferation of digital finance across countries, most models are not new. Many organisations are simply “copy and pasting” their models from another country or provider and not innovating.

Furthermore, a majority of providers are still having trouble convincing their clients to use the service; in 2015, only 10 percent of mobile connections linked to mobile money accounts in the countries where it was offered. The bulk of mobile money transactions (93 percent of volumes and 87 percent of values ) are still limited to three categories: airtime top-up, bill pay and person-to-person transfers, which means that providers have not yet been able to convince customers to diversify their usage, and therefore product development is limited. It is time for the next stage of evolution, but many providers are still focused on selling basic products to existing clients and struggling to build their agent networks.

In retrospect, the industry is moving much slower than many of us hoped when it began over a decade ago. Exciting innovation is happening, it is just mostly happening elsewhere. Technology firms in places like San Francisco, New Delhi, Shanghai and London are raising billions of dollars in investment, expanding rapidly and introducing new approaches to finance that have the potential to shift the foundations of the industry.

This fintech innovation started with a focus on developed-world markets but has already flowed into emerging markets like India and China. As these initial markets become more saturated and digital connectivity improves in the developing world, fintech companies will shift their focus in search of new markets for growth.

The mobile money and agent banking markets of the developing world will likely be disrupted, and providers would be wise to prepare for this now. In a newly released paper from the Helix Institute of Digital Finance, titled “Redesigning Digital Finance for Big Data”, we begin by offering a framework of analysis for understanding the myriad of different players in the fintech world.

We recommend that regardless of individual digital financial providers’ decisions to cooperate or compete with these new market entrants, they will all be better positioned if they begin focusing on developing the asset which serves as the common denominator and foundation for all financial technology companies. That foundation is data. The crux of the fintech model is to develop complex algorithms that can predict consumer behaviour, everything from the customer service they need to the ability to repay a loan or the next purchase they are likely to make. However, these algorithms are only as good as the databases they are based on.

While banks and telecoms already possess unique and important customer data, which is already being used in some cases to provide small loans and other services, the datasets are far from complete. Therefore, there is ample opportunity to improve the market value of datasets by both expanding their size while also customising them to meet the needs of different types of fintech players.

To do this, digital finance providers need to increase the number of customers they have using their services as well as the frequency with which they are used.

This newly released paper maps out four practical shifts digital finance providers should make in their strategic operations to refocus themselves from short-term transactional revenue to long-term growth in this impending shift in market dynamics.

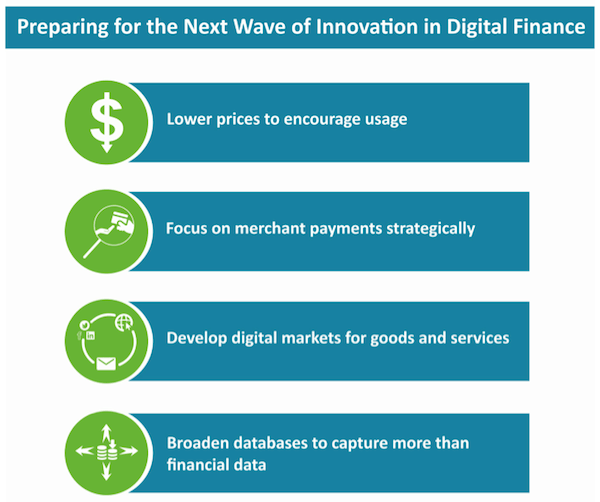

In summary, they are:

- Lower prices to encourage usage, and then shift the revenue model to higher-margin activities while lowering distribution costs.

- Focus on merchant payments strategically in categories of businesses that have shown adoption. This is because merchant payments are relatively frequent compared to other payments categories and therefore will add valuable customer data to the system.

- Develop digital markets for goods and services, as this has already been shown to be an important part of the future of retail, and leading players are making significant inroads in the developing world.

- Broaden databases to capture more than financial data. This involves more proactive data collection, and possibly partnerships with other organisations that can help put together a complete customer profile.

Data has become an asset in a world where analytics are becoming increasingly good at making predictions that drive business. Those that do not invest in data seriously, run the risk of being left out of the next evolution in finance. While it is important for banks and telecoms to understand this from a business perspective, it is also vital for policymakers to ensure they are creating conducive environments for innovation, while also enacting customer protection policies that shield people from its misuse.

Please find the full text of the newly released paper, titled: “Redesigning Digital Finance for Big Data.”

Mike McCaffrey is an independent financial technology consultant and Annabel Schiff is a senior manager in market intelligence at Caribou Digital. They wrote this article, and the paper it describes, on behalf of The Helix Institute of Digital Finance.

Illustration courtesy of lucky_sun via Flickr. Homepage image credit: Grempz, via Flickr.

You May Also Be Interested In:

- Categories

- Technology